When you get down to it, real financial success in real estate boils down to one simple thing: positive rental property cash flow. This is the money that's actually left in your bank account after every single bill has been paid. It's the truest measure of your investment's health. For an expert Beaumont Property Management firm like ours, understanding your bottom line is everything. If you’ve ever wondered, "Can I hire a property manager for my house?", the answer is yes, and a professional partner is key to maximizing that profit. With a team providing expert Property management Beaumont services, you can navigate your investment with confidence.

The Real Meaning of Rental Property Cash Flow

If you've ever found yourself asking, "Can I hire a property manager for my house?", the answer is a definite yes—and understanding this concept is your crucial first step. For an expert Beaumont Property Management firm like ours, knowing the numbers is everything. Too many investors get caught off guard by hidden costs, but we build our strategy around stable, long-term rentals (leases of 6 months or longer) to create a predictable and profitable asset for you.

With an experienced partner providing Property management Beaumont services, you can navigate these details with confidence. Our team has been serving communities like Redlands, Beaumont, Calimesa, Yucaipa, Loma Linda, Mentone, Highland and Banning California since 1997. In that time, we've built a deep understanding of the local market. This guide will break down everything you need to know, from making accurate calculations to implementing powerful strategies to optimize your returns.

Why Cash Flow Is Your Most Important Metric

Think of cash flow as the heartbeat of your investment. Sure, property appreciation is a fantastic long-term goal, but you can't use potential future value to pay this month's mortgage or cover an unexpected plumbing disaster.

Positive cash flow is the monthly income that makes your investment sustainable. It's what separates a property that funds your life from one that drains your savings.

To really master this, it's essential to first understand how to track cash flow and get a handle on your money management. This is the foundation that separates the pros from the amateurs. A solid cash flow allows you to:

- Build a safety net: Cover surprise vacancies or major repairs without breaking a sweat.

- Reinvest for growth: Use the profits to pay down your loan faster, save for another property, or make smart upgrades that add value.

- Achieve financial freedom: Create that dependable stream of passive income that supports your long-term goals.

The Stability of Long-Term Leases

At AIM, we focus exclusively on long-term leases of six months or longer. This isn't by accident—it's a deliberate strategy designed to protect and enhance your cash flow. We do not provide services for short-term rentals.

Long-term rentals give you predictable income, dramatically lower the costs associated with tenant turnover, and reduce the general wear and tear on your property. This stability is the bedrock of any sound investment. For a deeper dive into another key metric, check out our guide on how to calculate rental yield.

Calculating Your True Profitability Step by Step

To really get a handle on your rental property cash flow, you have to look past the back-of-the-napkin math and get systematic. True financial clarity comes from tracking every dollar that comes in and every dollar that goes out. This isn't just about bookkeeping; it's about avoiding nasty surprises and making smarter, more confident investment moves.

The journey starts with your Gross Rental Income (GRI). This is the absolute maximum rent you could pocket if your property was rented out for all 12 months of the year. So, if your property rents for $2,000 a month, your annual GRI is a straightforward $24,000.

From that high point, we have to start subtracting all the costs that come with owning and running the place. These are your operating expenses.

Identifying Your Operating Expenses

Operating expenses are much more than just the mortgage. For a truly accurate picture, you need a complete list. Forgetting even one or two of these can paint a dangerously rosy and misleading view of your investment's health.

Here are the key expenses you absolutely need to track:

- Property Taxes: The annual bill from your local city or county.

- Insurance: This is your landlord or hazard insurance policy premium.

- Property Management Fees: For investors who want a hands-off experience, professional management fees are a critical line item. Our competitive 7.9% monthly fee is a perfect example.

- Maintenance and Repairs: You need a fund for both routine upkeep (like lawn care) and the things that inevitably break (hello, leaky faucet). A good rule of thumb is to set aside 1% of the property’s value each year for this.

- HOA Fees: If your property is part of a homeowners association, don't forget to factor in these monthly or annual dues.

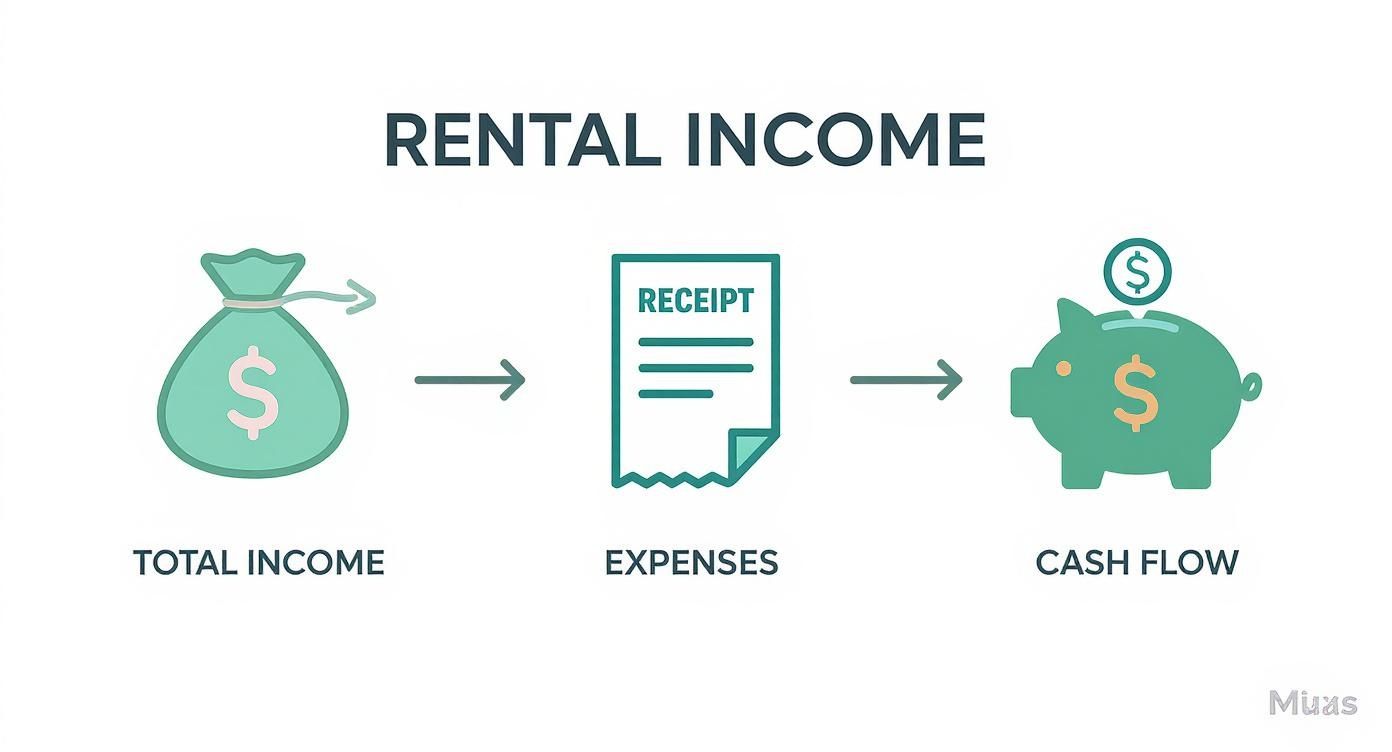

This infographic gives you a great visual of how the money flows from total income, through all the expenses, and down to your final cash flow.

As you can see, it’s really just a process of subtraction. You take all the money that comes in and subtract all the money that goes out. What’s left is your profit.

Calculating Net Operating Income and Final Cash Flow

Once you've tallied up every single operating expense, you can figure out your Net Operating Income (NOI). This is a hugely important number because it reveals how profitable the property is before you even consider your mortgage payments.

The Formula for NOI:

Gross Rental Income (GRI) – Total Operating Expenses = Net Operating Income (NOI)

NOI is a powerful tool. It helps you (and other investors) compare the performance of different properties on an apples-to-apples basis, no matter how they were financed. It's also a key ingredient when you learn how to calculate the cap rate on a rental property, which is another must-know metric for any serious investor.

The last step is to subtract your mortgage payment—which includes both principal and interest—to find out what your actual, take-home cash flow is.

Let’s walk through a real-world example of a single-family home in Beaumont to make this crystal clear.

| Sample Monthly Cash Flow Calculation |

| :— | :— | :— |

| Item | Amount | Notes |

| Gross Rental Income | $2,500 | The total monthly rent collected. |

| Operating Expenses: | | |

| Property Taxes | $300 | Your monthly property tax portion. |

| Insurance | $100 | Your monthly insurance premium. |

| Vacancy (5% reserve) | $125 | Setting aside funds for when the unit is empty. |

| Repairs (5% reserve) | $125 | Your monthly contribution to the repair fund. |

| Property Management (7.9%) | $197.50 | Fee for professional management services. |

| Total Operating Expenses | $847.50 | The sum of all non-mortgage costs. |

| Mortgage (P&I) | $1,300 | Your monthly loan payment (principal & interest). |

With these numbers, we can run the calculation. First, let's find the NOI:

$2,500 (GRI) – $847.50 (Expenses) = $1,652.50 (NOI)

Now for the final step, we subtract the mortgage to get our true cash flow:

$1,652.50 (NOI) – $1,300 (Mortgage) = $352.50 (Monthly Cash Flow)

In this scenario, the property is putting a positive cash flow of $352.50 into your pocket every single month. That’s the real profit you can use to save, reinvest, and build your wealth.

Decoding the Factors That Impact Your Bottom Line

Your rental property cash flow is never a fixed number—think of it more like a living, breathing metric that reacts to a blend of market forces and property-specific details. To protect and grow your profits, you need to get a handle on the key drivers that can either boost your margins or shrink them when you least expect it. Mastering these variables is what separates a reactive owner from a proactive, strategic investor.

The first set of factors is external, meaning they’re happening around your property. You can't directly control them, but you absolutely have to anticipate them. We're talking about things like shifting market rents in communities like Highland and Loma Linda, local vacancy rates, and the overall economic health of the area. A booming local economy often means higher demand for rentals and stronger cash flow, while a downturn can sink it fast.

Then, there are the internal factors—the ones tied directly to your property. These are the elements you have much more influence over, and managing them well is the secret to consistent income.

Property-Specific Drivers You Can Influence

The single most important internal factor is the quality and reliability of your tenants. A great long-term tenant who pays on time and cares for your property is the bedrock of predictable cash flow. On the flip side, a problem tenant can cause a cascade of issues—late payments, property damage, and expensive evictions that can wipe out months of profit in one go.

This is precisely why we only manage long-term rentals with leases of 6 months or longer. This strategy builds stability and minimizes the constant turnover and associated costs that eat away at an investor's bottom line. Consistent occupancy with a properly vetted tenant is always more profitable than the rollercoaster of short-term rentals.

Other critical property-specific elements include:

- Property Condition: A well-kept home attracts better tenants and lets you charge higher rent. Neglecting maintenance just leads to expensive emergency repairs that can destroy your cash flow.

- Operational Efficiency: How you manage the property day-to-day really matters. Smooth rent collection, quick maintenance responses, and clear communication all add up to a healthier financial picture.

A proactive approach to property management is non-negotiable. Anticipating maintenance needs and fostering positive tenant relationships directly protects your monthly income and prevents small issues from becoming major financial drains.

Understanding the Impact of Expenses and Financing

On the other side of the cash flow coin are your expenses, which can be just as unpredictable as your income. Unexpected cost increases can quickly turn a profitable property into a financial headache if you're not ready for them.

Key expenses to watch are rising insurance premiums, annual property tax reassessments, and sudden major repairs. A new roof or HVAC system can cost thousands, which is why it’s so important to maintain a healthy capital expenditure (CapEx) fund. This is money you set aside specifically for those big-ticket items.

Your financing structure also plays a massive role in your final cash flow. The interest rate and terms of your mortgage determine your monthly payment, which is often your biggest single expense. The broader financial climate has a direct effect here, too. For instance, when investors can get access to debt capital at competitive rates, it often helps boost cash flow by lowering those financing costs.

This is where a professional property manager helps you control these variables. By using established relationships with local vendors in communities from Beaumont to Banning, they can get cost-effective maintenance and repairs done right. Their expertise in tenant screening and lease enforcement minimizes income disruptions. A predictable, transparent management fee—like our low 7.9% monthly fee and flat $750 placement fee—is an investment that maximizes your net return. You can learn more about our property management fee structure to see how a clear and fair cost model contributes to a stronger bottom line.

Why Long-Term Rentals Build Sustainable Wealth

When it comes to building a real estate portfolio that actually generates wealth, not all rental strategies are created equal. The path you take has a huge impact on your rental property cash flow, your stress levels, and your ultimate success.

At AIM, we’ve focused exclusively on long-term leases—six months or more—since 1997. Why? Because it’s a strategy we’ve perfected to give our clients maximum stability and sustainable returns. We do not deal with short-term rentals.

This isn’t about chasing the highest possible nightly rate. It’s about building a reliable, hassle-free asset. The long-term model is designed for serious investors who value predictable income over the chaotic, high-maintenance world of short-term rentals. Let's dig into why this approach is the clear winner for lasting financial security.

The Power of Predictable Income

The biggest advantage of long-term rentals is simple: consistency. A tenant on a year-long lease provides a steady payment that arrives like clockwork every single month.

This reliability is the bedrock of strong cash flow. It lets you budget with confidence, cover your mortgage without sweating, and accurately project your profits for the year ahead.

Short-term rentals are the complete opposite. Your revenue can swing wildly based on the season, a local event, or even a single bad review online. That feast-or-famine cycle makes financial planning a nightmare and introduces a level of risk most smart investors want nothing to do with.

Drastically Reduced Operational Demands

Let's be honest: managing a short-term rental isn't really investing. It's running a hotel. The operational workload is intense and it never, ever stops.

Just think about the daily grind:

- Constant Marketing: You’re always hustling to fill the next vacancy, whether it’s for a weekend or a single week.

- Intensive Guest Communication: This means answering booking inquiries at all hours, coordinating check-ins, and being on-call 24/7 for guest issues.

- Frequent Cleanings: The property needs a top-to-bottom cleaning after every single guest. That's a huge cost in both time and money.

- Restocking Supplies: From toilet paper and soap to coffee and snacks, you are constantly replenishing amenities.

With a long-term rental, those headaches vanish. Once we place a quality tenant, your main job is done. We handle everything from rent collection to maintenance calls, letting you enjoy a truly passive income stream. The difference in day-to-day effort is monumental.

Lower Costs and Less Wear and Tear

The high turnover of short-term rentals also means significantly higher costs and much faster wear and tear on your property. Every guest changeover brings cleaning fees, marketing expenses, and the potential for damage from people who have no real stake in caring for the home.

Long-term tenants, on the other hand, treat the property like it's their own home. They’re far more likely to report maintenance issues quickly, take better care of appliances, and generally cause less damage. This translates directly to lower repair bills and a healthier bottom line.

The money saved from reduced turnover alone can give your annual cash flow a substantial boost. For a deeper dive into the numbers, check out our breakdown of short-term vs long-term rentals and what works best in Redlands.

To see the differences side-by-side, here's a quick comparison of how the two rental models stack up when it comes to cash flow.

Long-Term vs Short-Term Rentals: A Cash Flow Perspective

| Factor | Long-Term Rentals | Short-Term Rentals |

|---|---|---|

| Income Stream | Consistent & Predictable: Monthly rent payments from a single tenant. | Volatile & Seasonal: Revenue fluctuates based on demand, season, and occupancy. |

| Vacancy Risk | Low: Vacancies occur between long-term leases (e.g., once a year). | High: Constant risk of empty nights between guest stays. |

| Management | Low-Effort: "Set it and forget it" model once a tenant is placed. | High-Effort: Requires daily management, guest communication, and scheduling. |

| Operating Costs | Lower: Fewer turnovers mean less spending on cleaning and marketing. | Higher: Frequent cleaning fees, restocking supplies, and marketing costs add up. |

| Wear & Tear | Minimal: Tenants treat the property as their home, leading to less damage. | Accelerated: High foot traffic and guest turnover lead to more repairs. |

| Cash Flow | Stable & Reliable: Easier to forecast and build sustainable wealth. | Inconsistent: Potential for high peaks but also deep valleys. |

As you can see, while short-term rentals might promise higher gross revenue, the net profit is often eroded by higher costs and operational demands, making long-term rentals the more reliable path to positive cash flow.

By focusing on long-term tenants, you foster a sense of ownership and responsibility that protects your asset. This stability not only saves you money on repairs but also preserves the property's value over the long haul.

In communities from Redlands to Beaumont and Calimesa to Banning, we've seen this strategy deliver results for decades. It aligns perfectly with our goal: making property ownership profitable and stress-free for our clients by building robust investments designed for lasting returns, not fleeting profits.

Actionable Strategies to Boost Your Cash Flow

Knowing your numbers is one thing, but making them work for you is how you actually win at the real estate game. Boosting your rental property cash flow boils down to a simple, two-sided strategy: find smart ways to increase your income while trimming down your expenses.

With the right moves, you can turn a decent investment into a great one. These aren’t complex theories for Wall Street investors; they're practical, real-world steps any property owner can take. Let's dig into some actionable ways to make your property pull its weight.

Elevating Your Income Potential

The fastest way to improve your bottom line is to increase the revenue your property brings in. This doesn't have to mean shocking your tenants with a massive rent hike. Often, it's about making smart, affordable improvements that justify a better rental price and attract high-quality tenants who appreciate a well-cared-for home.

Think about these income-boosting ideas:

- Cost-Effective Upgrades: You don't need a gut renovation. Simple changes like a fresh coat of paint, new light fixtures, or modern cabinet pulls can make a huge difference in a property's appeal. For more inspiration, check out our guide on how to increase property value.

- Adding In-Demand Amenities: Depending on your market, adding a feature like an in-unit washer and dryer or even smart home tech can command a higher monthly rent.

- Implementing Fair Rent Increases: Keep an eye on the market rents in your area, from Redlands to Highland, and make sure your pricing is competitive. A small, justified annual increase keeps you profitable without driving away great tenants.

Strategically Reducing Your Expenses

Just as important as earning more is spending less. Every single dollar you save on expenses goes straight into your pocket as pure profit. This means being proactive with your finances, not just reacting when a bill comes due.

Start by looking at your largest recurring costs. Could you get a better deal? For instance, refinancing your mortgage when interest rates are favorable can slash your biggest monthly payment overnight.

One of the most powerful ways to cut costs is with a solid preventative maintenance schedule. Fixing a small leak today is infinitely cheaper than dealing with a catastrophic flood and mold problem down the line. It's about preventing those cash-flow-killing disasters.

Here are a few other powerful ways to trim the fat:

- Appealing Your Property Taxes: Tax assessments aren't set in stone. If you think your property has been overvalued, filing an appeal could lead to significant savings every year.

- Shopping for Better Insurance: Don't just auto-renew your policy. Get quotes from different insurance providers annually to ensure you're getting the best coverage for the best price.

- Efficient Property Management: A good management company should save you more than they cost. Our low 7.9% monthly management fee and flat $750 tenant placement fee are structured to maximize your net income. With experience dating back to 1997, we have deep-rooted, mature relationships with vendors in Beaumont, Calimesa, Yucaipa, and Banning, which means we get you better prices on maintenance.

Finally, think long-term. Big-ticket items like a new roof are inevitable. Exploring financing options for significant property repairs ahead of time keeps these capital expenditures from wrecking your budget and ensures your investment stays on a stable, profitable path.

Of course. Here is the rewritten section, crafted to sound completely human-written and natural, following the provided style guide and examples.

Your Questions on Rental Cash Flow Answered

Jumping into real estate investing brings up a lot of questions, especially around the numbers that actually drive your success. To help you move forward with confidence, we’ve put together answers to some of the most common questions we hear from investors about managing and optimizing rental property cash flow.

What Is a Good Cash Flow for a Rental Property?

While "good" is always a bit subjective, most seasoned investors I talk to aim for at least $100 to $200 in positive monthly cash flow for each unit—and that’s after every single expense is paid. This gives you a decent buffer and a real, tangible return you can feel each month.

Another way to look at it is the cash-on-cash return, which measures your annual cash flow against the actual cash you put into the deal. A healthy target here is usually somewhere between 8% and 12%. But honestly, the right number really comes down to your personal strategy.

For instance, in a hot market where property values are climbing, an investor might be perfectly happy with lower monthly cash flow, betting on a big payday when they eventually sell. On the flip side, if your goal is pure income, then maximizing that monthly profit is everything. You have to know your local market—from Calimesa to Mentone—to set goals that make sense with current property values, rents, and expenses.

How Can a Property Manager Increase My Cash Flow?

A great property manager does a lot more than just collect rent; they’re a profit optimizer for your investment. Their expertise hits both sides of the cash flow equation: they boost your income while strategically cutting your expenses.

They keep your income steady by minimizing vacancies. With smart marketing and a tough tenant screening process, they find reliable, long-term tenants fast, so your property isn’t sitting empty and bleeding money. They also have professional rent collection systems in place to ensure you get paid on time, every time.

At AIM, our experience since 1997 and our competitive low 7.9% management fee are all structured to improve your net income. We handle the day-to-day with seasoned efficiency, which directly fattens your bottom line.

Just as importantly, they slash your expenses by using their network of trusted, local vendors for maintenance. This means you get cost-effective repairs and avoid having small, cheap fixes turn into budget-wrecking disasters. Our mature relationships within the community translate into better service and pricing for you.

What Are the Biggest Mistakes That Kill Rental Cash Flow?

The three biggest cash flow killers I see are underestimating expenses, dealing with long vacancies, and making bad tenant choices. Any one of these can sink an otherwise solid investment.

New investors often budget for the big three—mortgage, taxes, and insurance—and stop there. They completely forget about routine maintenance, big-ticket capital expenses (CapEx) like a new roof down the line, property management fees, and the cost of an empty unit.

Speaking of which, an empty property is a pure liability. It's an expense machine, burning through cash every single month with zero income to show for it. This is exactly why we focus on long-term leases; that stability is crucial to avoiding this profit drain. We do not provide services for short-term rentals—our focus is on leases of six months or longer.

Finally, rushing to place a tenant without proper screening is a catastrophic mistake. One bad tenant can mean months of unpaid rent, serious property damage, and thousands in legal fees for eviction. That's a toxic cocktail that can wipe out years of profit. An experienced partner like AIM helps you sidestep these critical, wealth-destroying mistakes right from the get-go.

Ready to maximize your rental property's potential and achieve stress-free ownership? The team at AIM PROPERTY MANAGEMENT COMPANY has been helping investors in Redlands, Beaumont, Yucaipa, Loma Linda, Mentone, Highland, Calimesa, and Banning build sustainable wealth since 1997. Let our experience work for you.

Learn more about our professional property management services today!