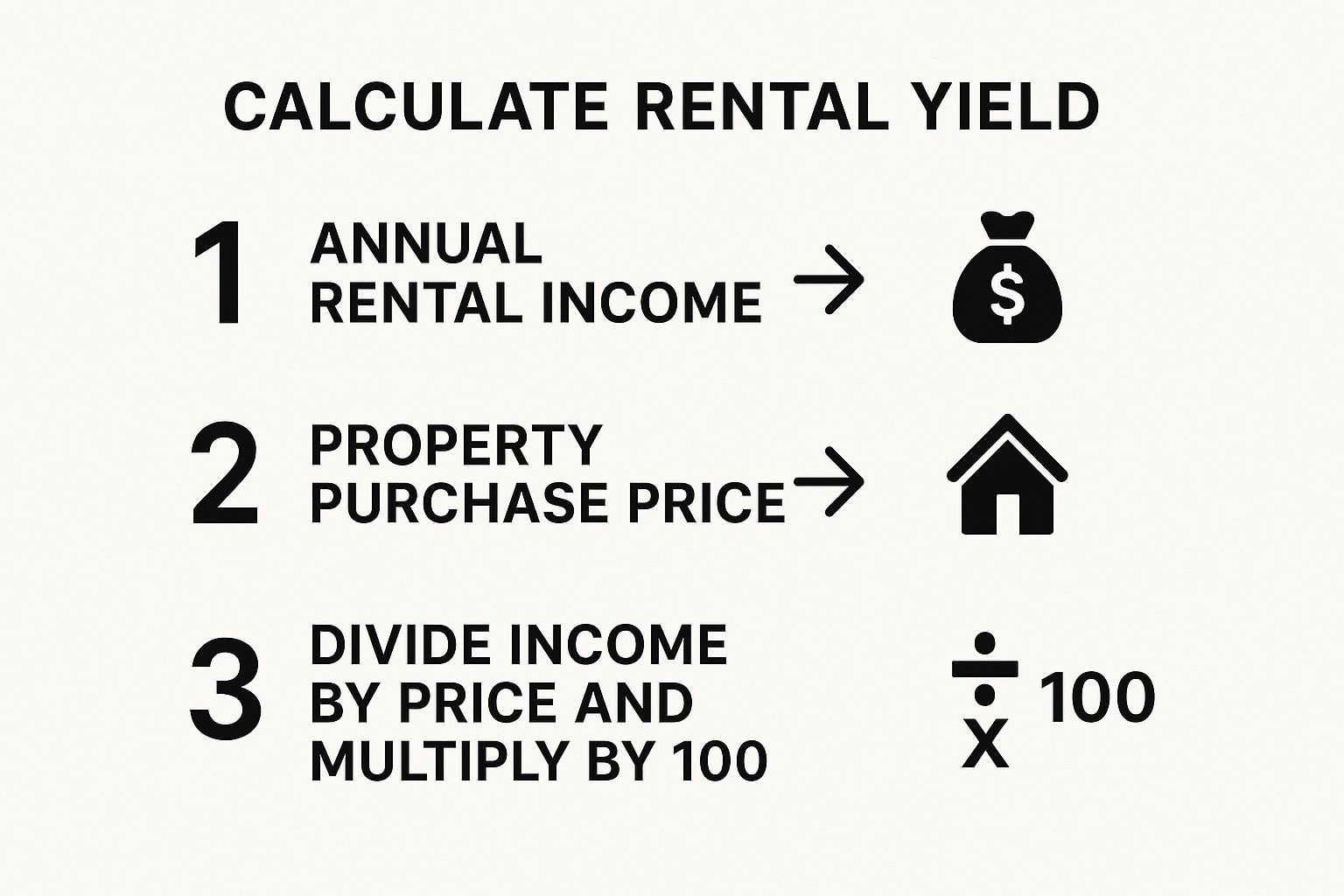

Before you even think about putting an offer on an investment property, you need a quick, reliable way to gauge its profitability. The simplest starting point is a basic rental yield calculation. All you do is take the annual rental income, divide it by the property's total purchase price, and multiply that by 100 to get a percentage. This little formula is your first-pass filter for comparing properties.

Why Rental Yield Is Your Most Important Metric

When you're looking at potential investments, you need a clear, objective picture of what you can expect in return. Rental yield gives you exactly that. It's truly the single most important metric for comparing different opportunities and understanding their real profitability, whether you're eyeing properties in Redlands, Beaumont, or Yucaipa.

Think of it as a universal yardstick. It cuts through the fluff and subjective opinions to give you a hard number representing your return on investment.

This percentage is so crucial because it forces you to make decisions based on data, not just a gut feeling. A property might look fantastic on the outside, but if the yield is low, it simply might not be the right fit for your financial goals. Calculating the yield lets you quickly see if a property is worth a closer look or if it's time to move on.

The Two Sides of Yield: Gross vs. Net

It's absolutely vital to understand that there are two ways to look at yield, and they tell very different stories.

- Gross Rental Yield is the quick-and-dirty calculation. It’s based only on rental income versus the property's cost. It's great for an initial screening but it definitely doesn't paint the full picture.

- Net Rental Yield is the figure that really matters. This one accounts for all the operating expenses that come with owning a property, revealing what you'll actually take home.

The gap between these two numbers can be surprisingly large. Industry data consistently shows that net yields are often 1.5% to 2% lower than gross yields because of costs like property taxes, insurance, and ongoing maintenance.

For a quick overview of the key differences, here’s a simple breakdown:

Gross vs Net Rental Yield At a Glance

| Metric | Gross Rental Yield | Net Rental Yield |

|---|---|---|

| Calculation | (Annual Rent / Property Value) * 100 | ((Annual Rent – Annual Expenses) / Total Investment) * 100 |

| Purpose | Quick, initial comparison of properties | Detailed, accurate measure of profitability |

| What It Shows | The property's income potential before costs | The actual return on your investment after all costs |

| Usefulness | Good for fast screening | Essential for final investment decisions |

So, a property that looks great with a 6% gross yield might only deliver a 4% net yield once you factor everything in. With the United States averaging a gross rental yield around 6.5%, knowing your real costs is essential for accurate forecasting and avoiding nasty surprises.

Understanding both gross and net yield is fundamental to building a successful real estate portfolio. One shows you the potential, while the other shows you the reality. Focusing only on gross yield is one of the most common mistakes new investors make.

Ultimately, your goal is to maximize your net return. That means not just collecting rent but actively managing your expenses and making smart improvements over time. If you're looking for actionable ideas, you might be interested in our guide on how to increase property value. By keeping your focus firmly on the net yield, you build a much more resilient and profitable investment strategy for the long term.

The Quick Guide to Gross Rental Yield

When you're first diving into potential investment properties, you need a fast, simple way to gauge its income potential. That's where gross rental yield comes in.

Think of it as your initial screening tool. It gives you a quick, high-level snapshot that helps you compare multiple properties without getting bogged down in the nitty-gritty details just yet. The goal here is to answer one simple question: how much income could this property generate relative to what it costs to buy it?

The calculation itself is refreshingly straightforward, which is why so many seasoned investors start here. You don't need a complex spreadsheet—just two key numbers.

The Simple Gross Yield Formula

To figure out the gross yield, you'll simply compare the total annual rent to the property's total acquisition cost.

The formula looks like this:

(Annual Rental Income / Total Property Cost) x 100 = Gross Rental Yield %

It’s crucial to use the total property cost, not just the purchase price you see on the listing. This figure should include the sale price plus any initial closing costs and immediate repairs needed to get the home rent-ready. Using this all-in number gives you a much more accurate baseline for your investment.

A Real-World Loma Linda Example

Let's put this formula into practice with a realistic scenario for a home in Loma Linda, California—a community we know well for its strong rental demand.

- Total Property Cost: You find a great single-family home and purchase it for $485,000. After factoring in closing costs and some minor updates (like new paint and carpet), your total investment comes to $500,000.

- Monthly Rent: Based on the local market, you determine a fair rent is $3,000 per month.

- Annual Rental Income: That's your monthly rent multiplied by 12, so $3,000 x 12 = $36,000.

Now, let's plug those numbers into our formula:

($36,000 / $500,000) x 100 = 7.2% Gross Rental Yield

This 7.2% figure gives you a solid starting point. You can now use this number to quickly compare this Loma Linda property against another one in Redlands or Highland to see which one looks stronger on paper. If you want more insights on spotting these kinds of opportunities, check out our guide on what makes a good rental property.

Remember, the gross yield is an optimistic number. It represents the property's earning potential in a perfect world with no vacancies, repairs, or management fees. It’s a valuable first look, but it’s not the final word on profitability.

This initial calculation is essential for filtering your options, but it completely ignores all the operational costs that will inevitably eat into your profit. That’s why the next step—calculating net yield—is where you uncover the real return on your investment.

Calculating Net Yield To Find Your Real Profit

Gross yield gives you a quick, back-of-the-napkin estimate, but it's the net rental yield that tells the real story. This is the number that separates a good-on-paper property from a genuinely profitable investment. Net yield cuts through the noise and shows you what you actually put in your pocket after all the bills are paid.

Trust me, ignoring operating costs is the fastest way to see a promising investment turn into a financial headache. To get your net yield, you have to be meticulous and account for every single cost of owning and running the property. This is how you move from a theoretical number to a real-world return.

Uncovering Your True Operating Costs

To get an accurate net yield, you need a complete picture of your annual operating expenses. These are the recurring costs that keep the property running, occupied, and compliant with the law.

Here's a list of the usual suspects you absolutely cannot forget:

- Property Taxes: A significant and unavoidable annual expense.

- Homeowners Insurance: Non-negotiable protection for your asset against damage and liability.

- Maintenance & Repairs: You need a fund for both routine upkeep (like landscaping) and the inevitable surprise fixes (like a busted water heater). A good rule of thumb is to set aside 1-2% of the property's value each year.

- Vacancy Reserves: No property stays occupied 100% of the time. It’s smart and conservative to budget for at least a 5% vacancy rate, which works out to about 18 days a year.

- Property Management Fees: The cost for a professional to handle the day-to-day, which is vital for maximizing returns and minimizing your own stress.

It's the expenses you don't plan for that hurt your bottom line the most. A detailed budget for net yield calculation is your best defense against unexpected financial surprises and ensures your investment performs as expected.

This visual gives a simple breakdown of the fundamental steps in any yield calculation.

As you can see, annual income and the property's price are the core of the equation. Net calculations just add that critical layer of real-world expenses on top.

Putting Net Yield Into Practice in Banning

Let's ground this with a real-world scenario in Banning, California. We'll use the same property from our gross yield example—a total purchase price of $500,000 and annual rent of $36,000. This is where we see how those operating costs drastically change the numbers and why competitive management fees matter so much.

Now, it's time to subtract the real annual expenses.

Sample Net Yield Calculation for a Banning Property

Here's a step-by-step breakdown of how the expenses stack up against the income for our Banning property.

| Item | Calculation | Amount |

|---|---|---|

| Annual Rental Income | $3,000 x 12 | $36,000 |

| Property Taxes | (approx. 1.25% of value) | -$6,250 |

| Homeowners Insurance | (annual premium) | -$1,500 |

| Maintenance Reserve | (1.5% of property value) | -$7,500 |

| Vacancy Reserve | (5% of annual rent) | -$1,800 |

| AIM Management Fee | (our low 7.9% of collected rent) | -$2,844 |

| Total Annual Expenses | -$19,894 | |

| Net Operating Income | $36,000 – $19,894 | $16,106 |

Once we have our net operating income of $16,106, the final calculation is simple:

($16,106 / $500,000) x 100 = 3.22% Net Rental Yield

And there you have it. The realistic return is 3.22%, which is a world away from the 7.2% gross yield we started with. This is the number that truly matters for your financial planning.

Our highly competitive 7.9% management fee makes a big difference here; a more typical 10% fee would have eaten another $756 from your net income, dragging the yield down even further. For those looking to get even deeper into their investment's profitability, understanding concepts like mastering margin calculations can be a huge advantage. This detailed, realistic approach is what ensures you're making decisions based on facts, not just optimistic potential.

The Long-Term Rental Advantage for Stable Returns

When you're trying to build real, sustainable wealth in real estate, the strategy you pick is everything. It’s easy to get lured in by the high nightly rates of short-term rentals, but that path often comes with a ton of volatility, constant turnover, and a need for intense, hands-on management.

If you’re looking for a more stable and predictable road to profitability, the smart money is on long-term rentals—the only kind we manage.

This approach is all about consistency. When you secure reliable, long-term tenants in communities like Calimesa and Yucaipa, you’re creating a dependable income stream that becomes the bedrock of your investment. You aren’t just filling a vacancy for a few weeks; you're building a stable financial asset for the long haul.

The Power of Predictable Cash Flow

The number one advantage of a long-term rental? Steady, predictable cash flow. A 12-month lease gives you a reliable revenue stream you can count on, month in and month out, unlike the wild swings of a vacation rental.

That consistency makes everything easier, from budgeting for your annual expenses to accurately forecasting your returns. It also cuts down on two of the biggest profit-killers in this business: vacancies and turnover costs.

- Minimized Vacancy: Longer leases mean fewer gaps between tenants, which keeps your annual income right where it should be.

- Lower Turnover Costs: You get to skip the frequent, costly cycle of deep cleaning, marketing, and re-keying that plagues short-term rentals.

- Reduced Management Burden: With a stable tenant in place, the day-to-day demands on your time and energy are dramatically lower.

This stability is exactly why seasoned investors—especially the ones we've worked with since our business was founded in 1997—almost always favor long-term strategies. It’s a proven model for minimizing risk and protecting your net yield.

For a serious investor, a property that produces consistent, hassle-free income is far more valuable than one that requires constant attention for fluctuating returns. Long-term rentals are about building a resilient investment, not just chasing peak-season profits.

Weathering Market Shifts and Economic Cycles

Let's be real—the rental market isn't immune to what's happening in the broader economy. Rental yields can and do get hit by macroeconomic cycles and market rent adjustments.

For example, after a huge post-pandemic surge that saw U.S. market rents jump an incredible 59% from 2019 levels, an influx of new supply and economic jitters caused a 5% drop in a single year. Locking in a long-term lease gives you a crucial buffer against that kind of volatility.

When you secure a rental rate for a full year or more, you insulate your cash flow from sudden market downturns, making your investment far more resilient. This is especially true when you have a property manager who really understands the local dynamics of areas like Redlands, Highland, and Banning.

On top of that, a lean operational structure is key to maximizing returns in any market. Partnering with a management company that offers a competitive fee structure—like our straightforward 7.9% monthly fee and $750 placement fee with no add-on fees—directly boosts your net yield by keeping more of your money in your pocket. You can learn more about how our property management services cost directly impacts your bottom line.

This kind of strategic advantage ensures your investment is optimized to perform, creating a stable foundation for long-term growth, no matter what the market throws at you.

How Smart Property Management Boosts Your Yield

When you calculate your net rental yield, one thing becomes painfully obvious: every single dollar you spend on operating costs eats directly into your profit. It’s no wonder so many investors see property management as just another line item on the expense sheet.

But that’s a limited view. Partnering with the right management company isn't a cost center at all—it’s an investment designed to protect and actively grow your returns.

Think of an experienced property manager as your on-the-ground asset manager. Their entire focus is on optimizing your property’s performance. This goes way beyond just collecting rent; we're talking about everything from setting the perfect rental price to handling proactive maintenance that stops small issues from spiraling into budget-killing emergencies.

Maximizing Your Income and Minimizing Costs

One of the fastest ways a great manager boosts your yield is by slashing costly vacancies. Having deep roots in the local community since 1997, we know the rental markets of Redlands, Beaumont, Calimesa, Yucaipa, Loma Linda, Mentone, Highland, and Banning inside and out. This isn't just trivia—it's the experience that allows us to price your property competitively to attract qualified tenants fast, cutting down the time your investment sits empty and unproductive.

Beyond just filling a vacancy, it’s about finding the right tenant. A rigorous screening process almost always leads to longer, more stable tenancies with fewer headaches. That’s why we’ve always prioritized the stability of long-term rentals over the unpredictable nature of short-term lets. Consistent occupancy is the bedrock of a healthy rental yield.

Controlling expenses is the other side of the coin. Our mature relationships with trusted local vendors mean we get quality maintenance and repairs done efficiently and at a fair price. This hands-on, proactive approach keeps your property in top-notch condition while reigning in the very costs that can otherwise bleed your net income dry.

A professional property manager's real value isn't just in the tasks they handle, but in the costly mistakes and vacancies they help you avoid. Their expertise is a direct investment in your property's long-term profitability and your own peace of mind.

The Financial Impact of a Lean Fee Structure

Of all your operating expenses, the property management fee is one of the biggest. That makes it a critical piece of your net yield calculation. A high fee can be a significant drag on your returns, even if the service itself is top-notch. This is where a competitive, transparent fee structure becomes a powerful advantage for an investor.

At AIM, we built our fee structure specifically to help you keep more of your earnings in your pocket.

- A Low Monthly Fee of 7.9%: The industry standard often hovers around 10% or even higher. Our lower fee, which is very competitive, directly translates to more net income for you, every single month.

- A Simple $750 Placement Fee: We keep tenant placement straightforward and affordable. You won't find any hidden add-on fees that pop up and surprise you later.

This lean approach ensures our services don't just add value through operational excellence but also through direct financial savings. By keeping your management costs low, your net rental yield is automatically higher, making your investment work that much harder for you.

If you're thinking about a partnership, our guide on how to find a good property manager is packed with valuable insights. At the end of the day, smart management is about creating a true partnership that turns your rental property into a genuinely optimized asset.

Answering Your Top Rental Yield Questions

After running the numbers and digging into the formulas, it's totally normal to have a few lingering questions. What do these percentages really mean for your bottom line? Let's clear up some of the most common questions we hear from property owners here in Redlands, Beaumont, and across the Inland Empire.

What Is a Good Rental Yield for an Investment Property?

This is the million-dollar question, and honestly, a "good" rental yield can feel like a moving target. It really depends on your location and what you're trying to achieve with your investment.

While you might hear that a gross yield between 5-8% is a decent benchmark, the number that truly matters is your net yield. That's your profit after all the bills are paid.

We generally see a net yield over 4% as a strong return in our market. But context is king. In a rapidly appreciating area, an investor might be okay with a lower initial yield because they're banking on the property's value to skyrocket. For most of us focused on steady, reliable income, a healthy positive cash flow is the main event.

The best way to judge a property’s yield is to stack it up against similar rentals in the same neighborhood. Local context is far more telling than any generic national average.

How Do I Factor in Vacancies When Calculating Yield?

Ignoring the possibility of vacancies is one of the fastest ways to get a nasty surprise. It's a real-world cost, and you absolutely have to bake it into your net yield calculation to get an honest financial picture.

A safe, conservative rule of thumb is to budget for a 5-10% vacancy rate. Think of it as losing about half a month to a full month of rent each year.

To apply this, just subtract that percentage from your potential gross annual rent before you start deducting your other operating costs. An experienced local property manager can give you a much more precise vacancy rate based on what's happening right now in cities like Mentone or Beaumont, which is invaluable for accurate forecasting. This also highlights why thorough tenant screening is so critical for minimizing turnover. You can learn more about what we look for by reading our guide on the top 5 tenant red flags every landlord should watch for.

Should I Use the Purchase Price or Market Value to Calculate Yield?

Great question. The answer depends entirely on what you’re trying to figure out. Each method gives you a different—but equally valuable—piece of the financial puzzle.

-

Use Purchase Price for "Yield on Cost." This tells you how well your initial investment is performing. When you want to know the return on the actual money you put into the deal (including closing costs and initial repairs), this is the number to use.

-

Use Market Value for Current Performance. This helps you understand how the property is doing today. It's the key to deciding whether you should hold on to it or sell. This calculation shows you the return you're getting on your current equity, which is crucial for making smart decisions about your portfolio's future.

For anyone looking at a new property to buy, always, always use the total expected purchase price to get the most accurate projection from day one.

Maximizing your net rental yield is about more than just numbers—it's about smart, proactive management. At AIM PROPERTY MANAGEMENT COMPANY, our experience since 1997 and our competitive fee structure are designed to put more of your rental income back in your pocket. Contact us today to learn how our dedicated team can help you achieve your investment goals.