If you're looking into buying rental property, one of the first terms you’ll hear tossed around is "cap rate." It sounds technical, but the concept is actually pretty simple. At its core, figuring out how to calculate cap rate on a rental property just involves dividing the property's Net Operating Income (NOI) by its current market value.

This single percentage gives you a quick, clean look at a property's potential return on investment, making it a go-to metric for comparing different opportunities on an apples-to-apples basis.

Your No-Nonsense Guide to Cap Rate

The capitalization rate, or cap rate, is your first look into a property's profitability. Think of it as a financial snapshot that strips away financing details—like a mortgage—to show you the raw earning power of the asset itself.

The formula is straightforward: Cap Rate = Net Operating Income / Property Value. Let's break down what each of those pieces really means for your analysis.

For a quick reference, here’s a simple breakdown of what goes into the formula.

Cap Rate Formula At a Glance

| Component | What It Is | What to Include/Exclude |

|---|---|---|

| Net Operating Income (NOI) | The property's annual income before mortgage payments. | Include: Rental income, parking fees, laundry income. Exclude: Mortgage payments, income taxes, depreciation, capital expenditures. |

| Operating Expenses | The day-to-day costs of running the property. | Include: Property taxes, insurance, utilities, maintenance, property management fees. Exclude: Loan principal and interest. |

| Property Value | The current worth of the property on the open market. | This can be the purchase price or a value from a recent appraisal or comparable sales analysis. |

Getting these numbers right is the key to an accurate calculation. Now let's dive deeper into the components.

Breaking Down the Formula

-

Net Operating Income (NOI): This is all the money your property brings in (mostly rent), minus all the necessary operating expenses. These are the real, day-to-day costs of keeping the lights on—think property taxes, insurance, routine maintenance, and property management fees. It’s what’s left before you pay the mortgage.

-

Property Value: This is usually the price you paid for the property. But if you've owned it for a while, you'd want to use its current market value, which you can find through a recent appraisal or by looking at what similar properties ("comps") in the area have sold for.

This calculation is fundamental for anyone looking to invest in long-term rentals, which has been the cornerstone of our business at AIM Property Management since we opened our doors in 1997. We've helped countless owners in communities like Redlands, Beaumont, Calimesa, Yucaipa, Loma Linda, Mentone, Highland, and Banning California build stable, predictable income streams by focusing on solid metrics like this.

Before you start crunching numbers, it helps to fully grasp the concept. If you need a more detailed primer, this guide on what is cap rate in real estate is a great resource.

Why This Metric Matters for Long-Term Rentals

The cap rate is especially powerful for evaluating long-term rental properties, which we define as leases of six months or longer. For example, if a property brings in an NOI of $50,000 and is worth $1,000,000, its cap rate is 5%. That tells you the property's unleveraged annual return.

The stability of a long-term lease provides a consistent income baseline, making your NOI—and therefore your cap rate calculation—far more reliable and predictable than the fluctuating revenues of short-term rentals.

Market conditions have a huge impact on what a "good" cap rate is. For instance, in the U.S. multifamily apartment sector, average cap rates shifted from 4.1% in 2021 to around 5.2% by early 2024 due to rising interest rates and other market changes.

Understanding these trends helps you set realistic expectations for your own investments, whether you're looking in Loma Linda, Highland, or Banning.

Nailing Your Net Operating Income Calculation

You can't get to an accurate cap rate without first locking down your Net Operating Income (NOI). This is the single most important variable in the entire formula, and frankly, it's where we see most new investors make mistakes that lead to bad deals and skewed expectations.

Think of NOI as your property's pure, unfiltered profitability—what it earns before any loans or financing come into the picture. The math is simple: start with all potential income, then subtract every single cost required to keep the lights on and the property running.

Identifying Your Gross Income

The starting point for your NOI is Gross Rental Income. For a long-term rental, this part is refreshingly straightforward: just take the monthly rent and multiply it by twelve.

This predictability is exactly why we exclusively manage long-term rentals at AIM, focusing on leases of six months or more. It provides a stable, consistent revenue stream you can bank on, unlike short-term rentals that get hammered by seasonal vacancies and fluctuating nightly rates. A long-term lease makes your income projections—and your cap rate—far more reliable.

Your NOI calculation needs to reflect the reality of owning an investment property. A precise, exhaustive list of operating expenses is non-negotiable for an accurate cap rate.

Subtracting Every Operating Expense

Once you have your gross annual income figured out, it's time to subtract your operating expenses. And I mean all of them. This goes way beyond just the obvious costs like taxes and insurance. A thorough accounting is absolutely critical here.

Some of the most common operating expenses you'll encounter include:

- Property Taxes: A significant and unavoidable annual cost.

- Landlord Insurance: Absolutely essential for protecting your asset from liability and damages.

- Maintenance and Repairs: You have to budget for routine upkeep, from a leaky faucet to an appliance on the fritz.

- Vacancy Reserves: Even with the best long-term tenants, it's smart to set aside a buffer (a common rule of thumb is 5% of gross rent) for the time between leases.

- Property Management Fees: For investors who want to be hands-off, this is a key expense. Our competitive 7.9% monthly management fee is a predictable cost that ensures your property is professionally handled without you lifting a finger.

The good news is that many of these expenses can be written off, which is a huge part of making your investment perform well financially. To get a better handle on what qualifies, check out our detailed guide to rental property tax deductions.

What Not to Include in Your NOI Calculation

Just as important as what you include is what you leave out. The NOI formula is specifically designed to measure how well the property itself performs on an operational level, completely separate from your financing or personal tax situation.

Because of this, you must exclude these items from your operating expenses:

- Mortgage Payments: Your loan payment, both principal and interest, is a financing cost, not an operating expense.

- Capital Expenditures (CapEx): These are big-ticket items that improve the property's lifespan, like a new roof or a full HVAC replacement. They aren't the same as routine maintenance.

- Income Taxes: Your personal or business income taxes have nothing to do with the property's day-to-day operational costs.

- Depreciation: This is a "paper" expense used for tax purposes. It's a non-cash deduction and doesn't impact your actual cash flow.

By carefully adding up all your income and subtracting only the true operating costs, you'll land on an accurate NOI. This number is the bedrock of a reliable cap rate, giving you the power to make sharp, informed investment decisions in communities from Redlands to Banning.

How to Determine Accurate Property Value

Now that we have the Net Operating Income (NOI) figured out, we need the other half of the puzzle: the property's value. Using an unrealistic value is a surefire way to get a misleading cap rate, so it’s crucial to ground this number in reality.

The right way to approach this depends entirely on where you are in your investment journey—whether you're looking at a new property or analyzing one you've owned for a while.

For a new acquisition, it's pretty straightforward. Your best bet is to simply use the purchase price. This is the hard, verifiable number you paid for the asset, and it's the most accurate "value" for your initial cap rate calculation.

But what if you've owned the property for years? Using the original purchase price is a classic mistake. Markets change, values fluctuate, and your property is likely worth something different today. For an accurate, up-to-date analysis, you need its current market value.

Finding Your Property's Current Market Value

Figuring out the current market value isn't just a guessing game; it takes a little bit of research into what’s happening in your local area. The most practical way to do this is by running a comparable sales analysis—what we in the industry call "looking at comps."

This just means finding recently sold properties that are a lot like yours in a few key areas:

- Location: Neighborhood is everything. A comp from Redlands won't tell you much about a property in Banning because the local market dynamics are completely different.

- Size and Features: Look for homes with a similar number of bedrooms, bathrooms, and overall square footage.

- Condition: Try to compare your property to others in a similar state of repair or with similar upgrades.

By seeing what these homes actually sold for, you can get a strong, evidence-based estimate of what your own property is worth. It's a technique we've been using since 1997 to help our clients in Yucaipa, Beaumont, and Calimesa understand how their assets are performing in the current market.

A property's value is never static. It's a direct reflection of the current market, driven by local demand, economic trends, and even interest rates. Using an old value will only give you an old, irrelevant cap rate.

When a Professional Appraisal Makes Sense

While running your own comps is great for getting a solid estimate, sometimes you need an official, unbiased number. That's when a professional appraisal is the way to go. An appraiser will give you a legally defensible and highly accurate assessment of your property's value after a thorough inspection and a detailed market analysis.

This step is often required if you're refinancing a loan or getting ready to sell. Having that official number ensures all your calculations are built on a rock-solid foundation, giving you real confidence in your investment strategy.

For proactive owners, taking a deep dive into how to increase property value can also give you actionable steps to boost your home’s market standing before an appraiser ever sets foot inside.

Ultimately, choosing a realistic and defensible value is non-negotiable for a meaningful cap rate. It makes sure your final number reflects today's market—not yesterday's price tag.

A Real-World Cap Rate Calculation in Action

Theory is one thing, but let's run the numbers on an actual property to see how this works in the real world. To really get a handle on how to calculate cap rate on a rental property, there's no substitute for a practical example.

Let's use a single-family home in Highland, California—a community we’ve been proudly serving since 1997.

First, we'll map out a simple profit and loss statement to find our Net Operating Income (NOI). After that, we'll pin down a realistic market value and plug it all into the formula. This is the exact process we use when helping our clients analyze potential deals across the Inland Empire, from Loma Linda to Banning.

Building the Income Statement

First up, let's nail down the income and expenses. This property is a long-term rental, which is the only type of property we manage at AIM. We stick to leases of six months or longer because it provides a stable, predictable income stream for our owners.

Here's the income side:

- Gross Annual Rent: The home rents for $2,800 a month. That gives us $33,600 per year.

- Vacancy Loss (5%): No property stays occupied 100% of the time. We always budget 5% for potential vacancy between tenants, which comes out to $1,680.

- Effective Gross Income: After accounting for vacancy, our realistic income is $31,920.

Now for the operating expenses—the real costs of owning the property.

- Property Taxes: We'll estimate these at $4,200 annually.

- Insurance: A standard landlord policy runs about $1,200 per year.

- Repairs & Maintenance: It's smart to set aside around $1,500 for the year.

- Tenant Placement Fee: This is a one-time fee to find a great tenant. Our straightforward placement fee is only $750 with no other add-on fees.

- Property Management Fee: We charge a competitive 7.9% of collected rent, which is a low fee compared to many other companies. This works out to $2,521.68 for the year ($31,920 x 0.079).

When you add all those up, our total operating expenses are $10,171.68.

To get our NOI, we just subtract the expenses from our effective income: $31,920 – $10,171.68 = $21,748.32.

Your Net Operating Income (NOI) is $21,748.32. This number is the property's annual profit before factoring in any mortgage payments. A precise NOI is the bedrock of a reliable cap rate calculation.

Calculating the Final Cap Rate

Okay, next we need the property's current market value. Based on recent comparable sales ("comps") in the Highland area, let's say this home is valued at $450,000.

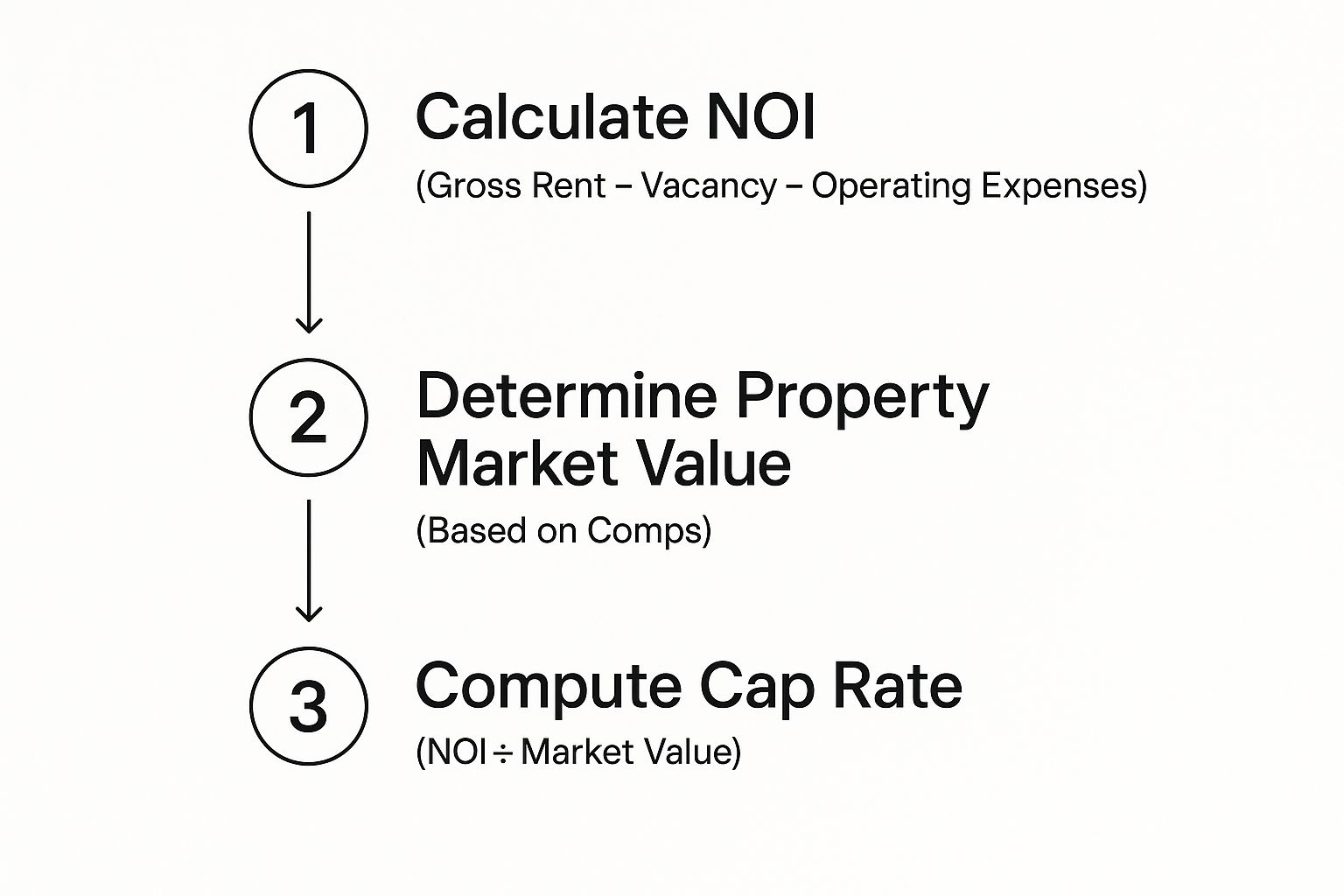

This simple infographic breaks down the three-step process, from gathering your numbers to getting the final cap rate.

As you can see, an accurate cap rate is a direct result of precise income calculations and a realistic property valuation. Now, we just have to do the division.

Cap Rate = NOI / Market Value

Cap Rate = $21,748.32 / $450,000 = 0.0483

To turn that into a percentage, just multiply by 100. The cap rate for this property is 4.83%.

While cap rate is a go-to metric, it's not the only way to measure performance. For another key calculation, check out our guide on how to calculate rental yield.

That 4.83% figure represents the property's annual return if you paid all cash (unleveraged). In the single-family rental world, cap rates are always shifting. Recent data shows average cap rates climbed from the mid-5% range to 6.8% by mid-2024, pushed up by interest rates and changing investor expectations. This just goes to show how cap rates reflect both a property's income and the broader market sentiment. You can read the full research about these SFR market dynamics to get more context.

Why We Champion Long-Term Rentals

The high nightly rates of short-term rentals look great on paper, but when you’re serious about building stable, long-term wealth, consistency is king. That’s why we focus exclusively on long-term leases of six months or more. It’s a strategy built for predictable returns and far less operational stress for you.

The biggest win? Consistent, reliable cash flow. A long-term tenant provides a steady income stream you can count on, making your Net Operating Income (NOI) solid and dependable. This is a world away from the seasonal ups and downs of short-term rentals, where a slow month can completely throw off your financial projections.

Lower Costs and Higher Returns

With long-term tenants, your operational costs drop significantly. Think about it: less turnover means you’re not constantly paying for cleanings, marketing campaigns, and the administrative hassle of finding a new guest every few weeks.

This is where our fee structure really shines for property owners.

Our $750 placement fee, for example, is a one-time cost with no other add-on fees. When you spread that over a 12-month lease, it delivers incredible value compared to the endless, recurring fees of managing short-term bookings. Pair that with our low 7.9% monthly management fee, and you have a structure designed to maximize what you actually keep in your pocket—boosting your cap rate in the process.

The stability you get from a long-term rental isn't just financial. It means less management stress and reduced wear and tear on your property. This approach also helps foster a real sense of community in neighborhoods like Mentone, Calimesa, and Yucaipa, which is something we deeply value.

To give you a clearer picture, here’s how the two strategies stack up.

Long-Term vs Short-Term Rentals: A Comparison

| Factor | Long-Term Rentals (Our Focus) | Short-Term Rentals |

|---|---|---|

| Income Stream | Consistent, predictable monthly payments | Variable, seasonal income with high volatility |

| Vacancy Risk | Low, with leases securing income for months | High, with gaps between guests and off-season lulls |

| Management | Less intensive, more hands-off for the owner | Daily, hands-on management and guest communication |

| Operating Costs | Lower; minimal turnover and marketing costs | High; frequent cleaning, restocking, and utility bills |

| Wear & Tear | Minimal, as tenants treat it like their home | Higher due to constant guest turnover |

| Regulations | Generally straightforward landlord-tenant laws | Complex, with local zoning and hotel tax rules |

As you can see, the long-term model is built for investors who prioritize stability and passive income over the high-maintenance demands of the short-term market.

A Proven Strategy for Stress-Free Returns

We’ve been in this business since 1997, and our entire model is built on providing stress-free property management. Our experience serving communities from Redlands and Beaumont to Loma Linda has shown us time and again that a long-term strategy is the superior choice for owners who want predictable returns without the chaos.

If you want to dive deeper into this, we break it all down in our article on short-term vs long-term rentals.

This long-term focus also aligns perfectly with smarter financing strategies. As you plan your investment, it pays to explore how different loan types can affect your returns, for example, by understanding financing options like DSCR loans. These loans are specifically designed for income-producing properties, which is an ideal match for the steady revenue you get from long-term leases in areas from Highland to Banning.

Common Cap Rate Mistakes and How to Avoid Them

A precise cap rate is an investor's best friend. A flawed one? It can lead you straight into a bad deal. The most common pitfall I see is investors drastically underestimating their operating expenses.

It's easy enough to remember the big stuff, like property taxes. But it’s the smaller, recurring costs that sneak up on you—things like vacancy rates, setting aside cash for future repairs, and budgeting for professional property management fees. These costs are very real, and they chip away at your Net Operating Income (NOI).

Forgetting them gives you a deceptively high cap rate that paints an overly rosy picture of the property's actual performance. Taking a look at a transparent property management fee structure can help you build these costs into your analysis from the start.

Using Inaccurate Property Values

Another frequent error is using an outdated or overly optimistic property value. Plugging in the price you paid for a property a decade ago just won’t cut it. The market has changed.

On the flip side, using an inflated list price instead of the true market value will artificially lower your cap rate, potentially making a great deal look less attractive than it really is.

To steer clear of this, always base your calculation on the current market value. You can determine this by looking at recent, comparable sales in the specific community you're analyzing, whether it's Redlands, Yucaipa, or Loma Linda.

Confusing NOI with Gross Rent

This is a critical mistake. Your Gross Rental Income is just the top-line revenue before a single bill gets paid. Using that number in the cap rate formula completely ignores the real costs of owning the property.

Doing this leads to a wildly inflated and frankly, useless metric.

Your cap rate is only as reliable as the numbers you feed into it. A disciplined, realistic analysis prevents you from turning a powerful tool into a simple vanity metric.

Forgetting Market Context

Finally, you have to remember that a "good" cap rate isn't some fixed, universal number. It lives and breathes with the market.

Historically, cap rates fluctuate with broader economic cycles. For instance, right after the 2008 financial crisis, cap rates were high because of the perceived risk in the market. They then steadily declined over the next decade, hitting historic lows of around 4.5% between 2020 and 2022.

By 2024, rising interest rates had pushed average multifamily cap rates back up to about 5.75%—the highest they'd been since 2014. Context is everything. Understanding these trends is key to knowing whether the deal in front of you is a winner or not.

Common Questions About Cap Rate

When you're digging into property analysis, a few questions about cap rate always seem to pop up. Let's tackle some of the most common ones I hear from investors.

What Is a Good Cap Rate for a Rental Property?

This is the million-dollar question, but the honest answer is: it depends. There's no magic number that works everywhere.

A "good" cap rate is all about context. In high-demand, pricier markets like you'd find across California, seeing a 4-6% cap rate is pretty standard. The lower rate reflects the high property values and the stability investors expect from that market. On the other hand, in different parts of the country, an investor might not even look at a property unless it’s hitting 8-10% or higher.

The best way to use cap rate is as a comparison tool. Instead of chasing a universal number, see how a property’s cap rate stacks up against similar properties in that exact same neighborhood. That’s where you'll find the real story.

Does the Cap Rate Calculation Include My Mortgage Payment?

Nope, and that's on purpose. The cap rate formula is designed to ignore any debt on the property, like your mortgage payment.

Think of it this way: cap rate measures the raw, unleveraged performance of the property itself. It tells you how well the asset generates income on its own, which is crucial for making apples-to-apples comparisons. It lets you evaluate two properties based purely on their operational health, without getting tangled up in how different investors decide to finance them.

How Does a Property Management Fee Affect My Cap Rate?

Property management is a core operating expense, so it has a direct impact on your Net Operating Income (NOI). When you factor in a management fee, your NOI goes down, and that, in turn, lowers your cap rate.

This is exactly why keeping operating costs under control is so important. An efficient, competitive management fee—like our low 7.9%—helps protect your bottom line. By minimizing expenses, you keep your NOI as healthy as possible, which translates directly to a stronger cap rate and a better-performing investment.

Maximizing your rental property's performance starts with expert management. At AIM PROPERTY MANAGEMENT COMPANY, our experience since 1997, combined with our low 7.9% monthly management fee and transparent $750 placement fee with no other add-on fees, ensures your investment is in trusted hands. We provide services only for long-term leases of 6 months or longer and do not deal with short-term rentals. Our mature relationships with the community serve Redlands, Beaumont, Calimesa, Yucaipa, Loma Linda, Mentone, Highland, and Banning California. Discover how our dedicated services can enhance your investment returns.