When you’ve built significant wealth, thinking about what happens next isn't just a good idea—it's absolutely essential. High net worth estate planning is the art of creating a strategic blueprint for your legacy, ensuring the assets you've worked so hard for are managed and transferred exactly as you wish.

This goes far beyond a simple will. It's a comprehensive plan designed to protect your fortune from being chipped away by taxes, legal battles, and the often messy and public probate process. Without it, even the most impressive portfolios are left vulnerable.

Why a Legacy Blueprint Is Non-Negotiable

For anyone with substantial assets, a standard, off-the-shelf estate plan just won't cut it. The complexity of your wealth—from a portfolio of investment properties and business interests to sophisticated financial instruments—demands a much more robust and detailed approach.

A well-crafted plan gives your family clarity and security. It ensures the wealth you’ve built will continue to support the people and causes that matter most to you for generations to come. This has never been more critical. We are currently in the middle of the largest intergenerational wealth transfer in history, with over $105 trillion expected to change hands in the U.S. alone over the next 25 years. You can learn more about this historic shift at CEP-DC.org. High-net-worth families are at the very heart of this transfer, and they are increasingly turning to advanced structures like trusts and family partnerships to keep their legacies intact.

Beyond a Simple Will: The Core Differences

Thinking about your estate as a collection of assets is one thing; structuring it to last for generations is a completely different ballgame. Real estate, in particular, requires specialized attention.

For many successful investors in communities like Redlands, Yucaipa, and Loma Linda, rental properties form the bedrock of their wealth. Managing these assets for the long haul starts with a deep understanding of their unique challenges. Knowing what makes a good rental property is the foundational first step in building a real estate portfolio that will endure.

The gap between a basic estate plan and one built for significant wealth is massive. The table below breaks down just how different the approach needs to be.

Key Differences Between Standard and High Net Worth Estate Planning

This table highlights why a specialized strategy is non-negotiable when substantial assets are involved.

| Planning Aspect | Standard Estate Plan | High Net Worth Estate Plan |

|---|---|---|

| Primary Goal | Asset distribution after death | Wealth preservation and tax minimization |

| Key Documents | Will, Power of Attorney | Advanced Trusts, LLCs, FLPs, Will |

| Tax Focus | Minimal focus on taxes | Federal estate tax, gift tax reduction |

| Asset Types | Simple assets (home, bank accounts) | Complex assets (businesses, real estate) |

| Privacy | Often public via probate court | Maintained through private trusts |

As you can see, the focus shifts dramatically from simple distribution to multi-generational preservation.

Ultimately, high net worth estate planning is about playing the long game. It tackles complex tax laws head-on, shields your assets from potential creditors, and leaves a crystal-clear, legally sound roadmap for your successors. It’s the final, definitive step in transforming your financial success into an enduring legacy.

Building Your Financial Fortress with Advanced Trusts

When you're dealing with significant wealth, moving beyond a basic will isn't just a good idea—it's the first step in serious high net worth estate planning. To truly safeguard what you’ve built, you need to construct a financial fortress. Advanced trusts are the foundational building blocks for that fortress.

Think of these legal instruments as more than just documents. They are powerful, active tools designed to give you control, privacy, and lasting protection.

A simple will is like having a gate to your estate. It serves a purpose, but it leaves your assets wide open to the public, costly, and painfully slow probate process. Trusts, on the other hand, are the high walls and reinforced structures that shield your wealth from those exact vulnerabilities.

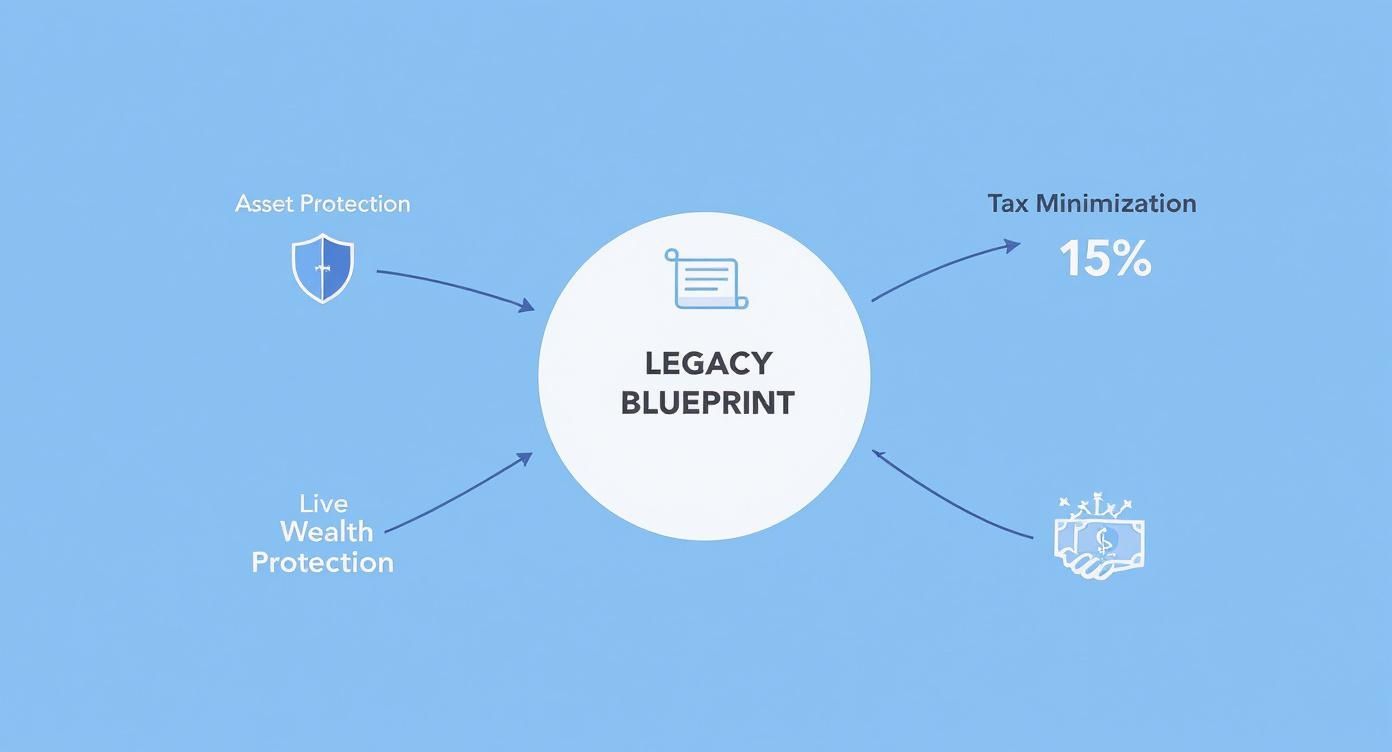

This diagram shows how a well-designed plan pulls together all the key pillars—asset protection, tax minimization, and wealth transfer—into one cohesive strategy.

As you can see, these goals aren't separate. They're deeply interconnected, with each piece reinforcing the others to create an estate plan that can truly stand the test of time.

Revocable Living Trusts: The Key to Avoiding Probate

For most people building their financial fortress, the journey begins with a Revocable Living Trust. It’s the most common starting point for a reason. During your lifetime, you keep total control over any assets you place inside it—you can add, remove, or change them whenever you want. It’s like having a secure vault where you’re the only one with the key.

When you pass away, a successor trustee you’ve already chosen steps in. They manage and distribute the assets exactly as you instructed, completely sidestepping probate court. This simple move delivers two massive advantages:

- Privacy: Probate is a public affair. A trust keeps your family's finances private, away from prying eyes.

- Efficiency: Skipping probate saves your heirs an incredible amount of time, money, and administrative headaches.

Irrevocable Trusts: The Ultimate Asset Shield

While a revocable trust offers flexibility, an Irrevocable Trust provides the ultimate level of protection. Once you transfer assets into this kind of trust, you generally can't change the terms or take the assets back. That might sound restrictive, but it's exactly what creates a powerful legal separation between you and your wealth.

By placing assets into an irrevocable trust, you effectively remove them from your personal balance sheet. This makes them inaccessible to future creditors and can significantly reduce the size of your taxable estate—a critical goal in high net worth estate planning.

This separation is where the magic happens. Because the assets are no longer legally yours, they are shielded from lawsuits and can fall outside the reach of federal estate taxes. For anyone with substantial assets, it's crucial to understand the different types of trusts available. You can learn more about the significant irrevocable trust tax benefits and how they can protect your legacy.

Specialized Trusts for Specific Goals

Beyond these foundational trusts, a whole toolbox of specialized instruments exists to tackle unique planning needs. Think of each one as a specific tool designed for a particular job in fortifying your legacy.

One of the most effective is the Irrevocable Life Insurance Trust (ILIT). An ILIT is created for one purpose: to own a life insurance policy. When you pass away, the death benefit is paid directly to the trust, not your estate. This provides your heirs with immediate, tax-free cash to cover estate taxes, debts, or other expenses without forcing them to sell off other valuable assets, like real estate or a family business.

By combining these instruments—a revocable trust to avoid probate, an irrevocable trust for asset protection, and an ILIT for liquidity—you create a multi-layered defense. This comprehensive structure ensures your financial fortress can withstand legal challenges, tax liabilities, and other unforeseen threats, preserving your wealth for generations to come.

Strategic Tax Reduction for Wealth Preservation

For high-net-worth families, tax planning isn't just about saving a few dollars here and there—it's about strategically protecting a legacy. The real goal isn't just to lower your tax bill for one year; it's to build a smart, durable framework that safeguards your assets for generations to come. Without a plan, a huge chunk of your wealth could be lost to federal and state taxes, shrinking the inheritance you've worked so hard to build.

This is where foresight and a solid understanding of the tax landscape come into play. It involves using proven legal and financial tools to reduce your taxable estate while staying true to your long-term goals.

Leveraging Lifetime Gifting and Tax Exemptions

One of the most effective tools in high-net-worth estate planning is the simple act of giving. The federal government allows you to give away a significant amount of assets—either during your life or at death—without triggering gift or estate taxes. This is your federal estate tax exemption.

Right now, that exemption is a major focus for many families. For 2025, it's a generous $13.99 million per person, but this number is set to drop dramatically soon. Because of this, many wealthy families are moving quickly to make large lifetime gifts and set up irrevocable trusts to lock in today's favorable rules.

Making gifts now allows you to move assets—and, just as importantly, all their future growth—out of your taxable estate. Not only does this cut down your potential estate tax bill, but it also gives you the joy of seeing your family benefit from your generosity while you're still here. For anyone with significant assets, implementing effective strategies to minimize estate taxes is absolutely essential for protecting wealth.

Advanced Tax-Reduction Instruments

Beyond just giving money away, there are specialized trusts designed specifically for tax reduction. Think of these as sophisticated tools for transferring wealth with minimal tax impact.

A Grantor Retained Annuity Trust (GRAT) is a fantastic way to pass on asset appreciation completely tax-free. Here’s the basic idea:

- Fund the Trust: You put appreciating assets, like stocks or real estate, into a trust for a specific number of years.

- Receive Annuity Payments: During that time, the trust pays you back a fixed annuity.

- Transfer the Growth: When the term ends, any growth on the assets above a certain IRS-set interest rate goes to your beneficiaries, completely free of gift and estate taxes.

A GRAT essentially "freezes" the value of your assets for estate tax purposes. It allows you to pass on all the future growth to your heirs, making it an excellent strategy for high-growth assets in a portfolio.

Philanthropy as a Tax Strategy

For many families, giving back is a core value and a central part of their legacy. The good news is that these philanthropic goals can align perfectly with powerful tax-reduction strategies through specialized charitable trusts.

Two of the most popular options are:

- Charitable Remainder Trusts (CRTs): You donate assets to a trust, which gives you (or someone you choose) an income stream for a set period. Once the term is up, the rest goes to your favorite charity, and you get an immediate income tax deduction.

- Charitable Lead Trusts (CLTs): This is the reverse. The charity gets an income stream from the trust for a set term. At the end, the remaining assets pass to your heirs, often with major gift and estate tax savings.

These strategies let you support causes you're passionate about while shrinking your taxable estate. For investors with significant real estate holdings, understanding how to manage tax liabilities is key. You can check out our guide on how rental property tax deductions can fit into a broader tax-reduction plan.

By combining these different methods, you can create a powerful, multi-faceted approach to wealth preservation that secures your family’s future and fulfills your charitable vision.

Managing Complex Assets in Your Estate Plan

In today's world, wealth isn't just about stocks, bonds, and a savings account. For many successful individuals, an estate plan has to grapple with a much wider, more complex range of assets—everything from cryptocurrency and NFTs to a sprawling real estate portfolio. If these unique assets aren't handled correctly, a huge chunk of your legacy can be left unprotected and become a massive headache for your heirs to sort out.

A smart high net worth estate planning strategy needs to create a clear roadmap for every single asset you own. This is especially true for two areas that are notoriously mishandled: the ever-growing universe of digital assets and the foundational wealth-builder of real estate.

Securing Your Digital Legacy

We're talking about more than just social media accounts. Cryptocurrency, NFTs, online businesses, and even valuable domain names are now a new frontier in estate planning. Unlike a deed or a stock certificate, there's no paper trail. Access is locked behind passwords and encryption, making it nearly impossible for your family to find or control anything without your explicit instructions.

This is a glaring vulnerability in far too many estate plans. The concern is real and growing—a staggering 80% of high-net-worth individuals hold at least one type of digital asset that hasn't been properly addressed in their plan. Even worse, fewer than 25% have officially named a digital beneficiary. This is a critical oversight, especially as the global digital asset management market races toward $8.1 billion. You can dig deeper into these trends in this insightful estate planning report.

To protect your digital footprint, you absolutely must create a detailed inventory of every digital asset and leave clear, unambiguous instructions for a trusted fiduciary on how to access and manage them.

Real Estate Holdings and Succession Planning

For countless investors, particularly in communities like Redlands, Beaumont, Calimesa, and Yucaipa, real estate is the very cornerstone of their wealth. These tangible assets demand a specialized game plan for management, liability protection, and, most importantly, succession.

Two of the most powerful tools for this job are Family Limited Partnerships (FLPs) and Limited Liability Companies (LLCs). By moving your properties into one of these legal structures, you gain some serious advantages:

- Protect Your Personal Assets: It builds a legal wall between your properties and your personal wealth, shielding you from lawsuits or liabilities tied to a specific property.

- Simplify Management: It bundles all your properties under one roof, making them much easier to manage as a single, cohesive business.

- Streamline Gifting: You can gift shares of the LLC or FLP to your family members over time. This lets you gradually pass on wealth while you still maintain control.

For property owners, a well-structured entity is not just a legal shield—it's a succession tool. It transforms a collection of deeds into a cohesive, manageable business that can be passed down smoothly to the next generation, avoiding the conflicts that can arise when heirs inherit property directly.

The Advantage of Long-Term Rentals for Your Estate

When weaving real estate into a long-term estate plan, stability is the name of the game. That’s precisely why we at AIM Property Management focus exclusively on long-term leases of six months or more. It’s a strategy that offers clear benefits over the rollercoaster of short-term rentals.

Long-term rentals create a predictable, consistent income stream, which makes financial forecasting for your estate far simpler. They also result in less wear and tear on your properties and help foster better tenant relationships, protecting the asset's value for years to come. Since 1997, our experience managing properties in communities from Redlands and Beaumont to Calimesa, Yucaipa, Loma Linda, Mentone, Highland, and Banning has proven that this focus on stability is essential for building lasting real estate wealth. We handle all the tenant management complexities for a low 7.9% monthly fee and a simple $750 placement fee with no other add on fees, ensuring your investment remains a dependable pillar of your legacy.

Ultimately, getting the most value out of your real estate is a key part of preserving your estate. For more strategies on this, take a look at our guide on how to increase property value for sustainable, long-term growth.

Assembling Your Professional Estate Planning Team

Trying to create a sophisticated high-net-worth estate plan on your own is a recipe for disaster. It's not a solo project; it’s a team sport. You wouldn't ask your family doctor to perform open-heart surgery, and you shouldn't rely on a single advisor to navigate the complex maze of legal, tax, and financial challenges that come with significant wealth.

Building a cohesive team of specialists is the only way to ensure every angle of your legacy is protected. Each professional brings a unique perspective and a specialized skill set to the table. When they work together, they can spot opportunities and head off risks that any one of them might miss on their own.

The Core Members of Your Advisory Team

Your estate planning "dream team" should have several key players, each with a distinct and vital role. Think of them as the board of directors for your financial legacy, guiding your assets with precision and foresight.

- Trust and Estate Attorney: This is your legal architect. They are the ones who draft the foundational documents—like trusts, wills, and powers of attorney—that create the legal backbone of your entire plan.

- Certified Public Accountant (CPA): Your CPA is your tax strategist, plain and simple. Their job is to minimize income, gift, and estate taxes, making sure your plan is as tax-efficient as possible while keeping up with ever-changing regulations.

- Financial Advisor: This is the professional who manages your investment portfolio. They work to align your investments with your long-term estate planning goals, ensuring your assets are growing in a way that supports the legacy you want to leave.

- Insurance Specialist: An insurance expert is focused on your liquidity needs. They help structure tools like life insurance to provide tax-free cash for your heirs, so they can cover estate taxes and other bills without being forced to sell off valuable assets.

The Rising Demand for Proactive Guidance

In today's complex financial world, affluent families expect more than just reactive advice. They're becoming far more selective, showing a clear preference for advisors who offer proactive and responsive guidance.

Recent data shows that while 82% of wealthy households use a CPA, a staggering 40% are thinking about switching providers because they aren't getting enough forward-thinking advice. Even more telling, only about half of high-net-worth households even have a trust and estate attorney on their team—a huge gap considering the legal complexities of transferring wealth. You can see more of these trends in a recent high-net-worth household survey.

This shift highlights a critical point: high-net-worth families need a team that anticipates challenges and brings solutions to the table before problems arise. A passive advisor just won't cut it anymore when it comes to protecting a significant estate.

For real estate investors, this team often needs one more key specialist: a property manager. An experienced property management company acts as your on-the-ground expert, preserving the value of your real estate portfolio, which is often a cornerstone of the estate. Their role in maintaining income streams and property condition is indispensable.

Our guide on how to choose a property management company offers deeper insights into finding the right partner to protect your real estate investments. Assembling this full roster of experts ensures your financial legacy isn’t just planned for, but actively protected for years to come.

Costly Mistakes to Avoid in Your Estate Plan

Putting together a solid high net worth estate planning strategy is about more than just picking the right legal tools. It's just as much about dodging the common landmines that can blow up even the most well-intentioned plans.

Learning from where others have gone wrong is one of the smartest things you can do to protect your wealth and make sure your legacy unfolds exactly as you envision. A tiny oversight today can easily snowball into a massive, expensive headache for your heirs down the road.

Even with a top-notch team of advisors, simple human error has a way of creeping in. The most damaging mistakes usually aren't about complex legal theory; they're basic oversights that end up having huge consequences.

Failing to Fund Your Trust

This is, without a doubt, the most common and devastating mistake we see. You can spend thousands on a brilliantly drafted trust, but if you never legally transfer your assets into it—a process called "funding"—that trust is nothing more than an empty, useless stack of paper.

It’s like building a state-of-the-art vault but forgetting to put anything inside.

When a trust is left unfunded, all your assets, from your home to your investment accounts, are stuck outside of it. That means they will be forced through the public, expensive, and painfully slow probate process. Your heirs will be thrown right back into the exact mess you created the trust to avoid.

Neglecting Beneficiary Designations

Here’s something many people miss: several of your most valuable assets, like life insurance policies, 401(k)s, and IRAs, don't follow the instructions in your will or trust. Instead, they pass directly to whomever you named on the beneficiary designation form.

Forgetting to update these forms after a major life event can be catastrophic.

Just imagine this scenario:

- You name your spouse as the beneficiary on your large life insurance policy.

- Years later, you get divorced and remarry but never get around to updating that form.

- When you pass away, the entire life insurance payout could legally go to your ex-spouse. Your current spouse and children would get nothing from that asset, no matter what your will says.

Taking 30 minutes once a year to review these forms is a simple habit that can prevent a world of hurt. Just as crucial is ensuring your real estate assets are properly insured; our landlord insurance comparison for CA rentals can help you see how the right coverage is a key part of a complete asset protection strategy.

Overlooking Incapacity Planning

A good estate plan isn't just about what happens after you die. It must also have a clear plan for what happens if you're still alive but become incapacitated and can't make decisions for yourself.

Without the right legal documents in place—like a durable power of attorney for your finances and a healthcare directive—your family could be forced into court to have a guardian appointed for you.

This court process, often called a conservatorship, is public, emotionally draining for your family, and incredibly expensive. It puts a judge, not the people you trust, in control of your money and medical care. It's a situation almost everyone would want to avoid.

Mishandling Blended Family Dynamics

Blended families bring a layer of complexity that standard, off-the-shelf estate plans just can't handle. Without specific, crystal-clear instructions, it’s shockingly easy to unintentionally disinherit your children from a previous marriage.

A classic mistake is leaving everything to your new spouse, simply assuming they will take care of your children later on.

But once you’re gone, your surviving spouse is legally free to change their own will and leave all of your assets to their own children, a new partner, or anyone else they choose. The only way to guarantee your wishes are respected is by using legal structures, like certain types of trusts, that provide for your spouse while locking in your children's inheritance.

A Few Common Questions About Estate Planning

Diving into high-net-worth estate planning always brings up a few key questions. It's completely natural. As you start putting the pieces together to protect your legacy, getting clear, straightforward answers is the best way to move forward with confidence. Let's tackle some of the most common things that come up.

It's a conversation more and more people are having. The global estate planning services market is expected to jump from $318 million in 2025 to a staggering $503 million by 2032—a clear sign that people are recognizing its importance. Still, it's surprising that just over half of wealthy families actually work with a trust and estate attorney, leaving a big gap where professional guidance should be. You can find more details about the estate planning market on intelmarketresearch.com.

I Already Have a Will, So Do I Really Need a Trust?

In a word, yes—especially if you have significant assets. A will is a great starting point, but it has one major drawback: it has to go through probate. That's a public, and often expensive, court process. A trust, on the other hand, is private. It lets your assets be managed and passed on to your heirs efficiently, without any court interference.

Trusts also give you incredible control over how and when your heirs get their inheritance. This can be a powerful tool to protect those assets from creditors, divorces, or simply immature spending habits. For anyone with a high net worth, a trust isn't just an add-on; it’s the cornerstone of a solid plan.

How Often Should I Look Over My Estate Plan?

Think of your estate plan less like a stone tablet and more like a living blueprint for your future. It needs to change as your life changes. A good rule of thumb is to give it a thorough review every three to five years.

That said, you should call your attorney immediately after any major life event. Don't wait. These events include things like:

- Getting married or divorced, or welcoming a new child

- A major shift in your net worth (up or down)

- Buying or selling a business or a significant piece of real estate

- Changes in state or federal tax laws that could affect you

How Can I Protect My Real Estate Holdings in My Estate?

For real estate investors, protecting your properties is everything. The best way to do this is to place them inside a legal structure like an LLC or a Family Limited Partnership (FLP). Doing this builds a firewall between your personal wealth and any liabilities tied to your properties—a must-have for preserving your wealth over the long term.

Another key is to focus on stable, long-term rental income. This strategy not only creates a predictable cash flow that simplifies financial planning for your estate, but it also minimizes the wear-and-tear that comes with frequent tenant turnover. It’s a philosophy we’ve built our business on since 1997.

At AIM Property Management, we stick to what works. We exclusively manage long-term leases of six months or longer, as we do not provide services for short term rentals. This approach ensures your real estate assets in communities like Redlands, Loma Linda, and Beaumont provide consistent, reliable returns, making them a strong pillar of your legacy for years to come.

Ready to secure your real estate investments with a proven, long-term strategy? AIM PROPERTY MANAGEMENT COMPANY offers expert management with a low 7.9% monthly fee and a simple $750 placement fee. We have been serving the communities of Redlands, Beaumont, Calimesa, Yucaipa, Loma Linda, Mentone, Highland, and Banning, California since 1997. Let our experience work for your legacy. Visit us at https://aim-properties.com to learn more.