If you’re a landlord, a solid insurance policy isn't just a good idea—it’s the bedrock of a sound investment strategy. But not just any policy will do. A landlord insurance comparison is one of the most important steps you can take, because what you need is far different from a standard homeowner's policy. Landlord insurance is specifically built to cover property damage, liability, and loss of rental income, all of which are crucial for protecting your bottom line.

Why Landlord Insurance Is a Must-Have

It’s a common mistake for new landlords to think their homeowner’s insurance has them covered. That's a costly assumption. Homeowner's policies are designed for a house you live in, not a property you rent out as a business. The moment you start renting, it’s considered a commercial activity, and most homeowner’s policies will flat-out deny claims related to it.

Imagine a tenant gets hurt on the property or a fire causes significant damage. Without the right coverage, you’d be on the hook for every penny of medical bills, legal fees, and repair costs. Landlord insurance is designed to step in and handle these exact risks.

The Core Protections You Need

A good landlord policy really comes down to three key areas of coverage. Think of them as a safety net for your investment, each protecting you from a different kind of financial hit.

- Property Protection: This is the most obvious one. It covers the physical building—the house itself, the garage, fences—from damage caused by things like storms, fires, or even vandalism.

- Liability Coverage: This is huge. If a tenant or a guest is injured on your property and you're found negligent, this coverage helps pay for their medical expenses and your legal defense. A single slip-and-fall accident could be financially devastating without it.

- Loss of Income Security: What happens if a covered event, like a major kitchen fire, makes your property unlivable? This feature reimburses you for the rent payments you lose while the property is being repaired, so your cash flow doesn't stop.

Long-Term Rentals Mean More Stability

The type of tenants you have can also impact your risk profile—and your insurance options. At AIM Property Management, we exclusively focus on long-term rentals because they provide a level of stability that insurers love. With a long-term tenant, there's less turnover, fewer vacancies, and a reduced risk of the issues that come with short-term lets. This stability often makes it easier and more affordable to get great insurance coverage.

Securing a reliable, long-term tenant is one of the most effective strategies for mitigating risk and ensuring a predictable revenue stream for your property.

It's no surprise the global landlord insurance market is booming. Valued at $20.7 billion in 2023, it’s expected to hit $40.9 billion by 2032. This rapid growth shows that more and more property owners recognize specialized insurance is non-negotiable. Staying on top of your legal duties is just as important; our guide on landlord responsibilities in California is a great resource for owners in communities from Redlands to Banning.

Diving Into the Details: Comparing Key Landlord Insurance Coverages

When you start shopping for landlord insurance, it's easy to get fixated on the monthly premium. But the real value isn't in the price tag—it’s in the fine print. The truth is, not all policies are created equal. A subtle difference in wording can be the deciding factor between a fully covered claim and a massive out-of-pocket expense. Getting this right is fundamental to protecting your investment.

One of the first big decisions you'll face is choosing between Actual Cash Value (ACV) and Replacement Cost Value (RCV) coverage. Think of ACV as what your damaged property was worth the second before the incident, accounting for wear and tear. RCV, on the other hand, pays out what it costs to buy a brand new, similar item today. While RCV policies come with a higher premium, they give you the funds to actually rebuild and replace everything—a must-have in areas like Redlands or Yucaipa where construction costs don't leave much room for error.

Liability Limits and Real-World Scenarios

Liability coverage is what stands between you and a potentially devastating lawsuit. Imagine a tenant trips on a loose step at your Loma Linda property and gets injured. Your liability coverage is what pays for their medical bills and your legal defense. A standard policy might offer $300,000 in liability, but in today’s world, that might not be enough. We almost always recommend landlords opt for limits of $1 million or more, especially if you own more than one property.

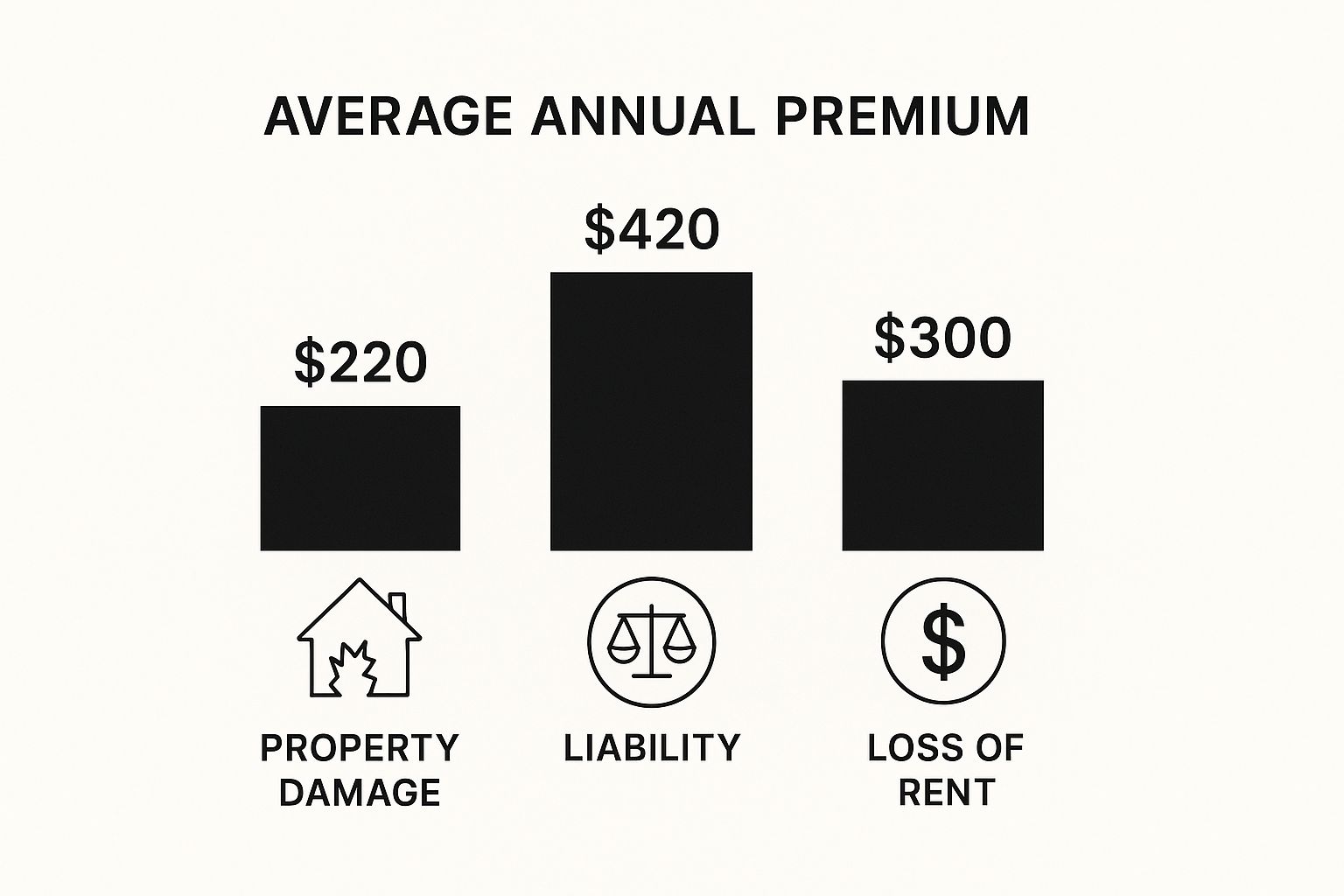

The infographic below breaks down how different coverages typically contribute to your annual premium.

As you can see, property damage makes up the biggest slice of the pie, simply because rebuilding is expensive. Liability and loss of rent are smaller but provide an essential financial safety net.

Unpacking Your Loss of Rental Income Coverage

Loss of Rental Income coverage is a lifesaver, but you need to know exactly how it works. This policy feature reimburses you for lost rent if your property becomes unlivable after a covered event, like a fire or a serious pipe burst. The devil is in the details here. You need to know what events trigger the coverage and for how long it will pay out. Some policies cap this at 12 months, while others might limit it to a percentage of your total dwelling coverage.

When you're comparing policies, don't be afraid to ask for specific, real-world examples of what triggers the loss of income coverage. A vague clause is a red flag that could leave you high and dry right when you need that rental income the most.

To help you get a clearer picture of what to look for, here’s a quick breakdown of the three main types of landlord insurance policies.

Landlord Insurance Coverage Comparison

| Coverage Type | Standard Policy (DP-1) | Broad Policy (DP-2) | Special Policy (DP-3) | Common Use Case |

|---|---|---|---|---|

| Dwelling Coverage | Named Perils Only (e.g., fire) | Broader Named Perils (e.g., falling objects, ice) | "All-Risk" (Open Peril); covers everything unless specifically excluded | A vacant property being renovated might only need a DP-1, while a high-value rental needs the comprehensive protection of a DP-3. |

| Personal Property | Named Perils | Named Perils | "All-Risk" (Open Peril) | Covers your property on-site, like appliances or lawn equipment. The DP-3 offers the most robust protection. |

| Liability | Often not included; must be added | Typically Included | Almost always included | Essential for any landlord. Protects against lawsuits from tenant injuries or property damage. |

| Loss of Rent | Usually ACV basis; Named Perils | RCV or ACV basis; Broader Perils | RCV basis; "All-Risk" | If a fire (covered by all) makes the unit uninhabitable, all three would pay. But if a burst pipe (not on DP-1) causes it, only DP-2 and DP-3 would cover you. |

Each policy level—DP-1, DP-2, and DP-3—offers a different degree of protection. Choosing the right one depends entirely on your property, your tenants, and your tolerance for risk.

Ultimately, making sure your policy is rock-solid and aligns with state laws is non-negotiable. It's smart to brush up on the specific landlord-tenant laws in California to ensure your coverage ticks all the legal boxes. Taking the time to get this right from the start protects your cash flow and the future of your rental business.

Understanding Your Landlord Insurance Costs

Let’s be honest: no one enjoys paying for insurance, but understanding what drives the cost is the first step to getting the right coverage without overpaying. The premium for your landlord insurance policy isn’t just a random number; it’s calculated based on several key factors. We’re talking about your property's location, its age, the type of construction, and, of course, the coverage limits and deductible you choose.

Here in the Inland Empire, from Yucaipa to Banning, local conditions play a massive role. If your property is near a high-risk wildfire zone or a floodplain, you can expect that to be reflected in your rates. Even things like local crime statistics can nudge your premiums higher.

A few things to keep in mind:

- Property Location: High-risk zones for wildfires or floods will always cost more to insure.

- Coverage Limits: The more protection you buy, the higher the premium. It's a trade-off.

- Deductible Amount: Choosing a higher deductible is a straightforward way to lower your annual cost.

As a rule of thumb, landlord policies generally cost about 15% to 25% more than a standard homeowner's policy. Why the hike? It comes down to the added risks of being a landlord, like tenant injuries on your property and covering lost rental income while the place is being repaired after a covered event.

On average, we see annual premiums landing somewhere between $2,100 and $4,000. Of course, some landlords get quotes as low as $700, while others with higher-risk properties might see numbers north of $8,300. Nationally, premiums have been on the rise, jumping about 20% in just one year, especially in markets hit hard by extreme weather. For a deeper dive into the numbers, check out this landlord insurance statistics report.

Key Factors That Influence Your Premium

Location is, without a doubt, one of the biggest drivers of your insurance cost. A rental property near a known wildfire area in Highland or a flood-prone part of Mentone will carry a much higher risk rating in an underwriter's eyes. This single factor can change your annual premium by hundreds, sometimes even thousands, of dollars.

The coverage limits and deductibles you select also have a direct impact on your bottom line. It's a simple seesaw:

| Factor | Impact on Premium |

|---|---|

| High Coverage Limits | Increases cost significantly |

| Higher Deductible Amounts | Reduces annual premium |

For example, simply raising your deductible from $250 to $500 could lower your premium by up to 10%. It means you'd pay more out-of-pocket if you file a claim, but it saves you money every year. It’s all about finding that sweet spot between what you can afford and the level of risk you're comfortable with.

Benefits of Professional Management

This is where having a professional manager like AIM Property Management can really pay off. We help control your costs by actively mitigating risk. Insurers love to see that you have a partner who enforces strict tenant screening, conducts regular inspections, and stays on top of maintenance—and our track record since 1997 speaks for itself.

An expert management strategy directly reduces the frequency and severity of claims, which can lead to lower insurance premiums over time.

Our low 7.9% monthly management fee and $750 placement fee are transparent, with no hidden add-on fees, so you get maximum value. We also focus exclusively on long-term rentals, which helps avoid the complicated underwriting that comes with short-term stays.

By balancing essential coverage with these cost factors, landlords in the Inland Empire can make smarter, more informed decisions. To get an even clearer financial picture, take a look at our guide on rental property tax deductions to see how you can optimize your investment returns.

Armed with this breakdown, you’re in a much better position to choose the coverage and deductibles that fit your budget and risk tolerance. Now you can apply these insights to lock in comprehensive landlord insurance that doesn’t break the bank.

Don’t forget that things like interest rates and inflation also play an indirect role by affecting rebuilding costs, which causes insurers to adjust premiums. It's a good practice to review your policy at every renewal and shop around for quotes to make sure your rates are still competitive.

This proactive approach is what keeps you ahead of the game as a landlord in the Inland Empire.

Long-Term Versus Short-Term Rental Insurance

The way you rent out your property has a massive impact on your risk profile, and insurance companies pay very close attention. A quick landlord insurance comparison shows that insurers treat long-term and short-term rentals as two completely different beasts. This is a critical distinction for property owners in communities like Redlands and Beaumont, where a stable, long-term tenant is the bedrock of a smart investment.

Insurers love predictability. Long-term rentals, with tenants on leases for a year or more, deliver just that. This model means less tenant turnover, fewer strangers coming and going, and a resident who is far more likely to treat the place like their own home. From an underwriter's viewpoint, that stability equals lower risk, which makes standard landlord policies easier to get and more affordable.

The Higher Risks of Short-Term Rentals

Short-term rentals, on the other hand, are a lot more like running a hotel. You have a constant revolving door of guests, which naturally increases the odds of accidents, property damage, and liability claims. A weekend guest simply doesn't have the same investment in caring for the property as a long-term tenant who has put down roots.

Because of this much higher risk, most standard landlord policies flat-out exclude coverage for short-term rentals. To get the right protection, owners of these properties usually need a more expensive and specialized commercial or "vacation rental" policy. These policies are built for the business-like nature of short-term letting, but they definitely come with a higher price tag.

Securing a long-term tenant is not just a rental strategy; it's a risk management decision. The stability of a long-term lease directly contributes to lower insurance costs and a more predictable revenue stream for your investment.

Aligning Your Strategy for Better Rates

Focusing on long-term tenancies is one of the most effective ways to keep your insurance costs down and simplify your life as a landlord. For property owners in areas like Calimesa, Yucaipa, and Loma Linda, this approach creates a much more stable foundation for their investment. You can learn more about the specific advantages by exploring what works best for rentals in Redlands and other local markets.

At AIM Property Management, we exclusively manage long-term rentals. This focus lines up perfectly with our goal of building stable, profitable investments for our clients. By steering clear of the high-risk, high-turnover model of short-term lets, we help property owners lock in better insurance rates and enjoy greater peace of mind. Our experience since 1997 in Highland, Mentone, and Banning has shown us time and again that a well-vetted, long-term tenant is the best asset a rental property can have. It’s a strategy that truly protects your investment for the long haul.

How Expert Property Management Reduces Your Risk

While a solid insurance policy is your ultimate safety net, smart property management is your first line of defense. When you partner with an experienced manager, you actively reduce the very risks that lead to insurance claims and drive up premiums. Insurance carriers love to see landlords who are proactive about risk mitigation, and nothing sends a clearer signal than professional management.

This all starts with diligent tenant screening. A thorough process that verifies income, credit history, and references is the bedrock of securing reliable, long-term tenants. Insurers see this stability as a huge plus, since consistent occupancy minimizes the risks that come with vacancies and high turnover.

A Proactive Approach to Asset Protection

Effective management goes far beyond just cashing rent checks. It's about a systematic approach to keeping the property in top physical condition, which directly lowers your risk profile and, in turn, your insurance costs.

- Proactive Maintenance: A professional manager addresses small issues—like a leaky faucet—before they spiral into a major water damage claim.

- Regular Inspections: Scheduled walkthroughs are key for ensuring lease compliance and spotting potential hazards, from a faulty smoke detector to a loose handrail, that could become a liability claim.

- Established Vendor Relationships: Having a network of trusted, vetted contractors means repairs get done quickly and correctly, preventing minor problems from escalating into expensive disasters.

This hands-on strategy turns property management from a line-item expense into a core part of your risk management. For landlords with properties in communities like Redlands, Beaumont, and Calimesa, this level of oversight is invaluable.

An experienced property manager doesn't just react to problems—they anticipate and prevent them. This proactive stance is highly valued by insurance carriers and can lead to more favorable premiums over time.

The Value of Experience and Fair Pricing

Since 1997, AIM Property Management has been serving the Inland Empire, including Yucaipa, Loma Linda, and Highland. Our long-standing presence in the community means we've built deep-rooted relationships and refined a proven process that protects our clients' investments. We focus exclusively on long-term rentals, which helps create the kind of stable and secure environment that insurers prefer.

We believe in a straightforward fee structure designed for maximum value. Our clients benefit from a low 7.9% monthly management fee and a $750 placement fee, with no hidden charges or confusing add-ons. While expert management significantly reduces your risk, understanding the typical property management costs is crucial for your overall investment strategy.

By choosing the right partner, you gain both peace of mind and a stronger financial future. Discover more about our approach to expert property management and how we can help safeguard your asset.

Common Questions About Landlord Insurance

When you're comparing landlord insurance policies, a lot of questions can pop up. Getting straight answers is the only way to feel confident you're making the right call. Here, we'll tackle some of the most common things California landlords ask, giving you practical insights to protect your investment.

Does My Policy Cover My Tenant's Belongings?

In a word, no. Your landlord policy is there to protect your property—the building itself—and your liability as the owner. It doesn't extend to your tenant's personal possessions.

This is exactly why it's a smart move to require tenants to have their own renter's insurance. Writing this requirement directly into your lease agreement adds a critical layer of protection for everyone involved and helps sidestep potential conflicts if something like a fire or break-in happens.

What’s The Difference Between ACV and RCV Coverage?

Understanding this distinction is a big deal when you're doing a landlord insurance comparison. Actual Cash Value (ACV) pays you for the value of your damaged property after factoring in depreciation. Think of it as what that 10-year-old roof is worth today, not what you paid for it.

On the other hand, Replacement Cost Value (RCV) covers the full cost to replace or rebuild with new materials of similar quality, without any deduction for age or wear and tear. RCV policies do cost a bit more, but they offer far better financial protection, ensuring you actually have the funds to rebuild properly after a major disaster.

Can a Property Manager Help Lower My Insurance Premium?

They absolutely can. A great property manager, like us here at AIM, is all about reducing risk, and that’s music to an insurance carrier’s ears. We've been serving landlords in communities from Redlands to Banning since 1997, and risk mitigation is at the core of what we do.

Our careful tenant screening, routine property inspections, and proactive approach to maintenance dramatically reduce the odds of a claim ever being filed. Insurers see professionally managed properties as a much safer bet, which often translates into better premiums for you. It's a smart investment that protects your asset while helping control your long-term costs.

The stability and oversight provided by a professional property manager are highly valued by insurance carriers. Our focus on long-term rentals in areas like Highland and Mentone further reduces risk, positioning your property as a more attractive asset to insure.

This is especially true when you partner with a company specializing in long-term rentals. That model is just seen as inherently less risky than short-term or vacation lets. By steering clear of the high tenant turnover that comes with vacation rentals, we help landlords maintain the kind of stable, predictable environment that insurers love.

Is Loss of Rental Income Coverage Always Included?

Not always, so you have to check. While 'Loss of Rental Income' coverage is a vital safety net, it’s typically included in more comprehensive policies (like a DP-2 or DP-3) but might be missing from a bare-bones DP-1 plan.

This coverage pays you for the rent you lose if a covered event, like a fire, forces your tenants to move out while repairs are made. When you're comparing policies, always confirm this is part of the package to make sure your cash flow is protected when you need it most.

Why Choose Professional Management for Peace of Mind?

Beyond just insurance, professional management gives you a complete solution for protecting your investment. At AIM, we've built our name on trust and deep experience right here in the Inland Empire. Our pricing is straightforward—a low 7.9% monthly management fee and a $750 placement fee with no surprises.

By focusing only on long-term rentals in communities like Loma Linda, Yucaipa, and Calimesa, we help you build a more secure and profitable investment. It’s a strategic choice that simplifies your insurance needs and adds a ton of stability to your rental property, letting you enjoy the rewards of ownership without all the day-to-day stress.

Partner with a team that has protected landlords' investments for over two decades. AIM PROPERTY MANAGEMENT COMPANY offers the expertise and local knowledge you need to thrive in the Inland Empire. Discover how our services can secure your property and maximize your returns.