Stepping into the role of a landlord is a significant financial move, transforming a property into a powerful income-generating asset. While the potential for long-term wealth is substantial, the path is filled with challenges that can quickly overwhelm unprepared owners. Success isn't about luck; it's about implementing a proven system from the very beginning. This guide is built to provide exactly that, offering practical, first time landlord tips that bypass vague theory and focus on actionable strategies.

We will cover the essential pillars of effective property management, from conducting ironclad tenant screenings and creating legally sound lease agreements to mastering California's specific landlord-tenant laws. You will learn how to set a competitive rental price, budget for inevitable maintenance, and establish professional communication protocols that protect your time and investment.

This article specifically focuses on the stability and consistent cash flow of long-term rentals (leases of six months or longer), a more predictable alternative to the volatile short-term market. For property owners in communities like Redlands, Beaumont, Calimesa, Yucaipa, Loma Linda, Mentone, Highland, and Banning, mastering these fundamentals is the key to minimizing risk and maximizing returns. Let’s dive into the core practices that will build your foundation for a profitable landlording business.

1. Screen Tenants Thoroughly: Your First Line of Defense

As a first-time landlord, your most crucial task is protecting your investment, and that begins long before a tenant moves in. Thorough tenant screening is your first and best line of defense. This isn't just about a quick credit check; it’s a comprehensive evaluation of an applicant's financial stability, rental history, and overall reliability. A meticulous, well-documented screening process is one of the most effective first time landlord tips for ensuring a stable, long-term tenancy, which minimizes vacancy and maximizes your return.

By establishing clear, written criteria and applying them consistently to every applicant, you not only find qualified tenants but also protect yourself legally. This process involves verifying income, checking credit history, running a background check, and speaking directly with previous landlords. Skipping this step can lead to late payments, property damage, and costly evictions. For example, a landlord in Seattle saved over $15,000 in potential eviction costs by discovering an applicant had three prior evictions through a comprehensive screening service.

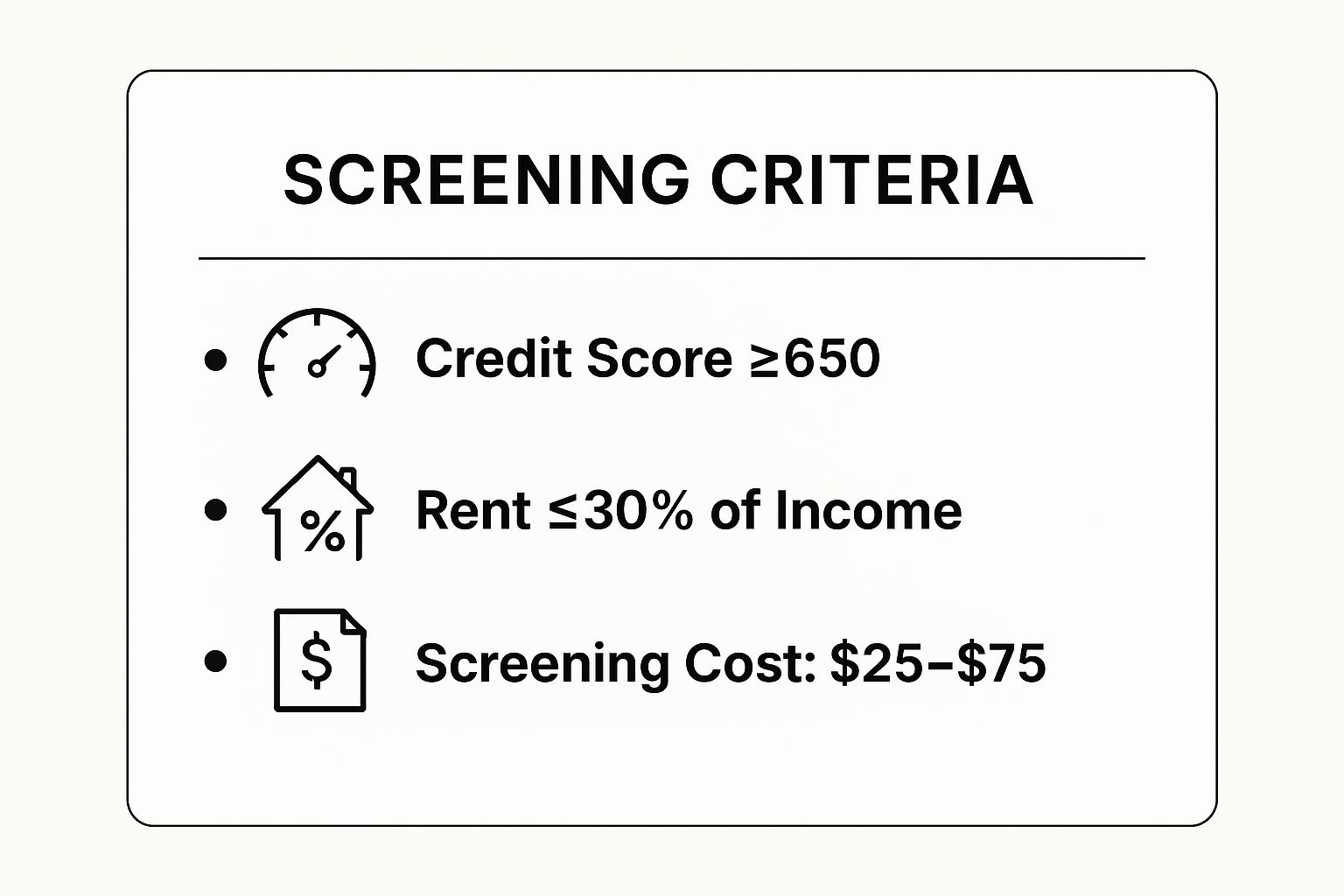

Key Screening Benchmarks

To streamline your process, focus on a few core financial metrics. These benchmarks help you objectively assess an applicant's ability to consistently meet their rental obligations.

Here is a quick reference guide summarizing common screening criteria used by property managers.

These metrics provide a strong, data-driven foundation for your decision, ensuring you select tenants who are financially prepared for a long-term lease.

Implementing Your Screening Process

Now, let's put this into action. A consistent process is vital for Fair Housing Act compliance.

- Establish Written Criteria: Before advertising your property, decide on your minimum requirements for credit score, income, and rental history.

- Use a Professional Service: Utilize established screening services like TransUnion or Experian to get a complete picture, including credit reports, eviction history, and criminal background.

- Verify Everything: Don't take applications at face value. Call employers to verify income and contact previous landlords with specific questions about payment history and property care.

- Charge a Screening Fee: Requesting a modest screening fee (typically $25-$75) ensures you only deal with serious applicants.

Mastering this single step sets the stage for a successful and profitable landlord experience. For a deeper dive into creating a foolproof vetting system, you can learn more about tenant screening made easy with AIM Property Management.

2. Create a Comprehensive Written Lease Agreement

Your lease agreement is the legal backbone of the entire landlord-tenant relationship. It's not just a formality; it's a legally binding contract that outlines every term, condition, and responsibility for both you and your tenant. A strong, detailed lease is one of the most essential first time landlord tips because it transforms ambiguous verbal agreements into concrete, enforceable rules. This clarity is your best tool for preventing disputes, managing expectations, and protecting your investment from potential misunderstandings.

A comprehensive lease serves as your primary reference for everything from rent payments and maintenance requests to property rules and eviction procedures. For instance, a first-time landlord in Florida successfully recovered thousands in pet damage costs specifically because their lease included detailed pet addendums and damage clauses. Without that written documentation, the financial loss would have been entirely theirs. Investing time in a thorough lease is far less costly than navigating a dispute without one, making it a critical step toward a stable, long-term rental business.

Key Lease Components

To ensure your agreement is comprehensive, it must cover all critical aspects of the tenancy. These clauses form the foundation of a secure and professional rental arrangement.

Here is a quick reference guide summarizing essential clauses for a strong lease.

These components eliminate ambiguity and provide a clear roadmap for the tenancy, protecting both parties and ensuring a smoother rental experience.

Implementing Your Lease Agreement

Now, let's put this into action. A well-executed lease is your most powerful legal tool.

- Use State-Specific Templates: Start with a template from a reputable source, like a state realtor association, to ensure it aligns with local laws.

- Consult an Attorney: Have a lawyer review your first lease. This initial investment can save you from significant legal trouble and financial loss down the line.

- Be Specific and Clear: Clearly define rent due dates, grace periods (e.g., 5 days), and the exact late fee amount. Detail maintenance procedures, specifying tenant and landlord responsibilities.

- Require Signatures and Initials: Ensure all adult occupants sign the lease. Having tenants initial each page confirms they have reviewed all terms.

A meticulously crafted lease sets clear expectations from day one, fostering a professional relationship built on long-term stability rather than the high turnover of short-term rentals. Beyond drafting a strong lease, understanding the specific legal framework, such as the Texas Lease Agreement Laws, is critical for compliance and protection.

3. Set the Right Rental Price Through Market Research

One of the most impactful first time landlord tips is mastering rental pricing through diligent market research. Setting the optimal rent is a careful balance; price too high, and your property sits vacant, costing you more than the extra rent would have generated. Price too low, and you leave significant money on the table each month. An effective pricing strategy ensures you maximize income while minimizing vacancy, attracting a strong pool of qualified applicants for long-term tenancies.

This process involves a deep dive into comparable local properties, analyzing their size, condition, and amenities against your own. A landlord in Denver, for example, reduced a 90-day vacancy to just 12 days by lowering the rent by a mere $50 per month based on market analysis. This small adjustment netted them an additional $3,600 annually by securing a stable, long-term tenant faster and avoiding the high turnover costs associated with short-term rentals.

Key Pricing Benchmarks

To avoid guesswork, ground your pricing decision in objective data. A comparative market analysis (CMA) is your best tool for understanding what the local market will bear.

Here is a quick reference guide for what to analyze when setting your rent.

These data points help you position your property competitively, ensuring it appeals to tenants seeking the stability of a long-term lease.

Implementing Your Pricing Strategy

A methodical approach to pricing will yield the best results. Follow these steps to determine your ideal rental rate.

- Analyze Comparables: Use sites like Zillow and Apartments.com to find 3-5 similar properties in your neighborhood. Note their rent, size, and amenities.

- Calculate Your Break-Even Point: Add up all your monthly costs (mortgage, insurance, taxes, maintenance fund, management fees) to determine your minimum required rent.

- Value Your Amenities: Adjust your price based on unique features. A washer/dryer can add $50-$100, while a newly updated kitchen might justify an extra $100-$200 per month.

- Be Ready to Adjust: If you receive no qualified applications within two weeks, it is a strong signal that your price may be too high for the current market.

Setting the right price is the first step in effective marketing. To learn how to present your well-priced property to the best tenants, you can explore more about how to advertise your rental property with AIM Property Management.

4. Understand and Follow Landlord-Tenant Laws

Beyond collecting rent, your role as a landlord is governed by a complex web of federal, state, and local laws. Understanding and strictly adhering to these regulations is non-negotiable. Landlord-tenant law dictates everything from security deposit handling and eviction procedures to property access and habitability standards. This legal framework is designed to protect both you and your tenant, creating a clear and enforceable rental relationship. One of the most critical first time landlord tips is to recognize that ignorance of the law is not a defense; a single misstep can lead to severe financial and legal penalties.

Violations can be costly and time-consuming. For instance, a California landlord was sued for $15,000 for improperly deducting from a security deposit and failing to provide an itemized list within the legal 21-day timeframe. By investing time to learn the rules upfront, you create standardized, legally compliant procedures for every aspect of your rental business. This not only protects you from lawsuits but also establishes you as a professional and fair landlord, attracting higher-quality, long-term tenants who appreciate a well-managed property.

Key Legal Compliance Areas

To build a legally sound operation, focus on several core areas where new landlords most often make mistakes. These pillars form the foundation of a compliant and defensible management strategy.

- Fair Housing: Strictly avoid any form of discrimination based on protected classes (race, religion, familial status, disability, etc.) in your advertising, screening, and management.

- Security Deposits: Know your state's specific limits on the amount you can charge and the exact timeline and procedure for returning funds after a tenancy ends.

- Property Entry: Understand the legal notice requirements (typically 24 hours written notice) for entering a tenant-occupied property for non-emergency reasons.

- Habitability: Fulfill your duty to provide a safe and livable home with functional essentials like heat, plumbing, and electricity.

Implementing Your Legal Framework

Now, let's put this knowledge into practice to protect your investment and ensure smooth operations.

- Consult a Professional: Before renting your property, have a brief consultation with a local landlord-tenant attorney to review your lease and procedures.

- Join an Association: Become a member of your local or state landlord association (like the American Apartment Owners Association) for access to legal forms, updates, and resources.

- Standardize Everything: Create written, standardized procedures for applications, maintenance requests, and notices. Apply them consistently to every applicant and tenant.

- Keep Meticulous Records: Document everything in writing, from initial inquiries and screening decisions to maintenance communications and rent payments.

Mastering these legal requirements is essential for long-term success. For a deeper understanding of the specific regulations in California, you can learn more about California landlord-tenant laws.

5. Build an Emergency Fund and Budget for Maintenance

Successful landlording is less about collecting rent and more about sound financial management. Your property is a business, and like any business, it will have unexpected expenses. Building a dedicated emergency fund and a proactive maintenance budget is one of the most vital first time landlord tips for protecting your investment from the inevitable costs of ownership, from a broken water heater to an extended vacancy. This financial buffer is what separates sustainable, long-term rentals from stressful, short-lived ventures.

Without proper reserves, a single major repair can wipe out years of profit or force you into high-interest debt. For example, a landlord who budgeted correctly was able to cover an $8,000 HVAC replacement without stress, using their emergency fund. In contrast, many new landlords are forced to sell at a loss when a major system like a roof fails unexpectedly. By planning for both routine upkeep and major capital expenditures, you ensure your property remains a profitable, appreciating asset rather than a financial liability.

Key Budgeting Benchmarks

To avoid being caught off guard, you need a clear financial strategy. Proactive budgeting removes the guesswork and helps you prepare for both small repairs and large-scale replacements.

Here is a quick reference guide summarizing common financial planning rules used by seasoned investors.

- Emergency Fund: Aim to save 3-6 months of total rental income to cover vacancies, evictions, or major surprise repairs.

- Routine Maintenance: Allocate 1-2% of the property's value annually for routine upkeep like plumbing fixes, paint touch-ups, and landscaping.

- Capital Expenditures (CapEx): Set aside an additional 1% of the property value each year for big-ticket items like a new roof, HVAC system, or appliances.

These financial benchmarks provide a solid framework, ensuring you have the capital needed to maintain the property and protect your cash flow.

Implementing Your Financial Safety Net

Now, let's put this into action. A disciplined approach to saving is non-negotiable for long-term success.

- Automate Your Savings: Treat your reserves as a fixed expense. Set up an automatic transfer to move 25-30% of each rent payment into a separate high-yield savings account exclusively for the property.

- Track Asset Lifespans: Know the age of your major systems. A roof typically lasts 20-25 years, an HVAC system 15-20 years, and a water heater 10-15 years. This helps you anticipate and budget for replacements.

- Prioritize Reserves Over Profit: In your first few years, focus on fully funding your emergency reserves before taking any profit from the rental income.

- Conduct Regular Inspections: Perform bi-annual inspections to identify and address small issues before they become expensive emergencies.

Proper financial planning is the bedrock of a stable rental business. To see how a professional property manager handles budgeting and maintenance for long-term rentals, explore how AIM Property Management builds sustainable investment strategies.

6. Conduct Regular Property Inspections

As a first-time landlord, a proactive approach to property maintenance is one of the most effective ways to protect your asset. Regular property inspections are your tool for proactive management, allowing you to catch small issues before they escalate into costly disasters. This isn't about spying on your tenants; it's a professional process to assess the property's condition, ensure lease compliance, and schedule preventative maintenance. Implementing a consistent inspection schedule is one of the most vital first time landlord tips for safeguarding your investment and fostering a positive, long-term tenancy.

Skipping this crucial step can lead to unpleasant surprises at move-out, such as discovering unauthorized pets, extensive property damage, or deferred maintenance that now requires thousands in repairs. For instance, one landlord discovered a slow leak under a bathroom sink during a semi-annual inspection, saving an estimated $15,000 in potential water damage and mold remediation costs. Regular inspections ensure your property remains a safe and well-maintained home, which is key to retaining great long-term tenants.

Key Inspection Benchmarks

To conduct effective and legally compliant inspections, you need a standardized process. This ensures you cover all critical areas of the property consistently and document your findings professionally, which is crucial for handling any security deposit disputes.

Here is a quick overview of what to focus on during different types of inspections.

These structured checks help you maintain the property's value and address tenant responsibilities in a timely manner.

Implementing Your Inspection Process

A well-documented inspection process protects both you and your tenant. Consistency and clear communication are essential for building trust and complying with state laws.

- Create a Standardized Checklist: Before the first walkthrough, develop a detailed checklist covering every room, appliance, and system. To ensure your property remains in top condition and to help budget for ongoing upkeep, consider using a downloaded comprehensive rental property maintenance checklist.

- Provide Proper Notice: Always give tenants written notice before an inspection, typically 24-48 hours, as required by your state's laws. This respects their privacy and ensures compliance.

- Document Everything: Use photos and videos to document the property's condition at move-in. This creates an undisputed baseline for comparison at move-out.

- Address Issues Promptly: If an inspection uncovers a maintenance need, address it quickly. This shows you are a responsible landlord and encourages tenants to take care of the property.

By making inspections a routine part of your management strategy, you ensure your investment is protected. For more insights into how this ties into your overall strategy, you can learn about why regular property maintenance is key for rentals.

7. Get Proper Insurance Coverage and Form an LLC

Beyond daily management, protecting your assets is a foundational task for any property owner. Standard homeowner's insurance is inadequate for rental properties, and your personal assets are vulnerable without a legal shield. This is where landlord insurance and a Limited Liability Company (LLC) create a critical two-part defense. This combination is one of the most vital first time landlord tips for safeguarding your financial future against property damage, tenant lawsuits, and other unforeseen liabilities.

Landlord insurance is specifically designed to cover risks associated with long-term rental activities, which a homeowner's policy will deny. Meanwhile, forming an LLC separates your personal wealth from your business assets. For instance, if a tenant's guest sues for a slip-and-fall incident, an LLC can limit their claim to the assets held by the company, protecting your personal home and savings. This dual-layer strategy is essential for the stability and security required for long-term rental success, which avoids the high turnover and liability risks of short-term rentals.

Key Risk Management Benchmarks

To build a robust financial and legal shield, focus on these core components. These benchmarks help you objectively protect your investment from common and catastrophic risks.

Here is a quick reference guide summarizing common protections used by experienced property investors.

These metrics provide a strong, multi-layered foundation for risk management, ensuring you are prepared for unexpected events.

Implementing Your Protection Strategy

Now, let's put this into action. A proactive approach to legal and financial protection is non-negotiable.

- Secure Landlord Insurance: Never use a homeowner's policy. Obtain a specific landlord policy that includes property damage, liability (at least $1 million), and loss-of-rent coverage.

- Form an LLC: Consult an attorney to establish an LLC in the state where your property is located. This creates a legal barrier between your rental business and personal assets.

- Maintain Separation: Keep business and personal finances entirely separate. Use a dedicated bank account for all rental income and expenses to maintain the LLC's liability protection.

- Require Renter's Insurance: Make it a lease requirement for tenants to carry their own renter's insurance. This covers their personal belongings and provides them with liability coverage, reducing your risk.

Building this protective framework is a crucial step toward sustainable, long-term rental income. For a more detailed breakdown of policy options, you can learn more about comparing landlord insurance policies for your property.

8. Establish Clear Communication Systems and Response Protocols

For a new landlord, a major pitfall is inconsistent or unprofessional communication, which quickly leads to tenant frustration and costly turnover. Establishing clear communication systems and response protocols from day one is essential. This isn't just about being friendly; it's about creating a documented, professional framework for all interactions, from routine maintenance requests to true emergencies. This is one of the most critical first time landlord tips for building strong tenant relationships and protecting your investment legally.

By defining how and when you will communicate, you set firm boundaries and manage expectations effectively. A structured system ensures all requests are tracked, response times are predictable, and a paper trail exists for every conversation. For instance, a property manager in California protected themselves in a dispute over an alleged unreported repair because their policy required all maintenance requests to be submitted in writing through a tenant portal. This simple protocol saved them from potential liability and reinforced the importance of clear, documented communication.

Key Communication Benchmarks

A proactive communication strategy prevents small issues from escalating. Defining your methods and response times upfront eliminates ambiguity and demonstrates professionalism, which is crucial for retaining high-quality tenants who prefer a well-managed property.

Here is a quick reference guide to establishing your communication framework.

- Routine Inquiries: Use email or a tenant portal for non-urgent questions.

- Maintenance Requests: Require written submissions via a portal or dedicated email.

- Rent Reminders: Automate via text or email a few days before the due date.

- Emergencies: Provide a dedicated phone number for immediate contact.

These channels create an organized, efficient system that respects both your time and your tenant's need for responsiveness, fostering a stable long-term rental environment.

Implementing Your Communication Protocols

Putting a clear system into action is straightforward and highly effective. Consistency is the key to success.

- Create a Welcome Packet: Provide new tenants with a document outlining all communication methods, expected response times (e.g., 24 hours for non-emergencies), and what constitutes a true emergency.

- Use a Tenant Portal: Leverage free or low-cost software like TenantCloud or Zillow Rental Manager to centralize maintenance requests, rent payments, and announcements.

- Define "Emergency": Clearly state that emergencies are situations threatening health or property, such as major water leaks, no heat in winter, or security breaches, not a burnt-out lightbulb.

- Document Everything: After any important verbal conversation, send a brief follow-up email summarizing what was discussed to create a written record.

- Set Professional Boundaries: Inform tenants of your business hours (e.g., no non-emergency calls after 8 PM) to maintain a healthy work-life balance.

Mastering communication is fundamental to successful property management and a cornerstone of the professional services offered by experienced firms. To see how a seasoned team handles tenant relations, explore the communication best practices used by AIM Property Management.

First-Time Landlord Tips Comparison Guide

| Item | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Screen Tenants Thoroughly | Moderate – Requires process setup and compliance knowledge | Moderate – Screening fees $25-$75/applicant, background checks | Reduced non-payment risk, better tenant quality | Before leasing to ensure tenant reliability | Lowers eviction costs, protects property & tenants |

| Create a Comprehensive Written Lease Agreement | Moderate to High – Needs legal knowledge or attorney review | Moderate – Potential legal fees ($200-$500) | Clear contract protection, reduced disputes | Every tenancy to formalize landlord-tenant terms | Legally enforceable, clarifies rights & duties |

| Set the Right Rental Price Through Market Research | Moderate – Time intensive (4-8 hrs) for analysis | Low to Moderate – Research tools mostly free | Maximize income, minimize vacancy periods | Prior to listing to competitively price property | Optimizes cash flow and attracts quality tenants |

| Understand and Follow Landlord-Tenant Laws | High – Complex, varies by location, ongoing updates needed | Moderate to High – Legal consultation ($300-$800) | Legal compliance, fewer lawsuits, enforceable leases | Continuously, before and during tenancy | Protects against legal risks and penalties |

| Build an Emergency Fund and Budget for Maintenance | Low to Moderate – Financial planning required | High – Requires capital allocation and savings | Financial stability, timely repairs, crisis prevention | Continuous financial planning during ownership | Safeguards finances, maintains property value |

| Conduct Regular Property Inspections | Moderate – Scheduling and documentation effort | Low to Moderate – Time plus basic tools (camera, checklist) | Early issue detection, lease compliance enforcement | Periodically during tenancy | Reduces repair costs, protects deposits, deters neglect |

| Get Proper Insurance Coverage and Form an LLC | Moderate to High – Insurance shopping and legal formation | Moderate to High – $800-2,000/year insurance + LLC fees | Liability protection, legal asset separation | Before tenant move-in and ongoing | Limits personal risk, covers damages & income loss |

| Establish Clear Communication Systems and Response Protocols | Moderate – Setup multi-channel systems, establish protocols | Low to Moderate – Software tools may have subscription costs | Improved tenant relations, fewer disputes | Continuous throughout tenancy | Enhances responsiveness & tenant retention |

Take the Next Step in Your Landlord Journey

Embarking on your journey as a first-time landlord is a significant financial milestone, one that transforms a physical asset into a thriving business. The transition from homeowner to property manager requires a strategic shift in mindset, moving from simply maintaining a space to actively managing an investment. The foundational tips we've covered are the essential building blocks for that transformation.

By mastering these core principles, you're not just renting out a property; you're creating a system for success. You're building a business designed for resilience, profitability, and peace of mind.

From Tips to Action: Your Path Forward

The difference between a stressed-out property owner and a confident investor often comes down to proactive implementation. Let's distill these concepts into your most critical next steps:

- Fortify Your Foundation: Your lease agreement and tenant screening process are your first line of defense. Don't compromise on these. A comprehensive, legally-sound lease paired with a meticulous screening protocol prevents the vast majority of future problems. This is the single most important area to invest your time and attention.

- Systematize Your Operations: Create clear, repeatable processes for everything. This includes rent collection, maintenance requests, and routine inspections. Document your policies and communication protocols. Systems remove guesswork and emotional decision-making, ensuring you treat every situation with consistency and professionalism.

- Prioritize Financial and Legal Diligence: Treat your rental like the business it is. Establish an LLC for liability protection, secure the right landlord insurance, and diligently follow all federal, state, and local landlord-tenant laws. An emergency fund isn't optional; it's a critical tool that ensures a single unexpected repair doesn't derail your investment.

The Value of Long-Term Stability Over Short-Term Volatility

A key decision you'll face is your rental strategy. AIM Property Management exclusively focuses on long-term leases of six months or longer, and for good reason. While short-term rentals can seem appealing with their high nightly rates, they come with significant downsides: inconsistent income, higher vacancy rates, increased wear and tear from constant turnover, and complex local regulations.

In contrast, long-term rentals offer far greater advantages for a stable investment:

- Consistent Cash Flow: Enjoy predictable, reliable income month after month.

- Lower Turnover Costs: Save money on frequent cleaning, marketing, and screening.

- Better Property Care: Tenants who view a property as their home are more likely to care for it.

- Reduced Management Burden: Fewer tenant changes mean less administrative work and stress.

This stability is the bedrock of a successful and sustainable investment strategy, which is why it is our sole focus.

Ultimately, these first time landlord tips are designed to empower you. Whether you decide to self-manage or seek professional support, understanding these fundamentals is non-negotiable. Building this knowledge base allows you to manage your asset confidently or, if you choose to partner with an expert, to do so from a position of strength and clarity. Your real estate investment is a powerful vehicle for building wealth, and with the right approach, you can navigate your landlord journey successfully for years to come.

Ready to protect your investment and ensure a stable, profitable rental experience in Redlands, Beaumont, Calimesa, Yucaipa, Loma Linda, Mentone, Highland, or Banning? Let AIM PROPERTY MANAGEMENT COMPANY apply our community experience since 1997 to manage your property. With our transparent, low 7.9% management fee and a simple $750 placement fee with no add-ons, we focus exclusively on securing quality long-term tenants for your peace of mind. Contact AIM PROPERTY MANAGEMENT COMPANY today for a free consultation.